Does Democracy Pay?

At its core, sovereign borrowing is like any other kind of debt. A government takes money now and promises to pay it back later — typically with interest — through regular payments over time. Investors, in turn, demand higher interest (or “spreads”) when they think repayment is uncertain.

But with governments, the uncertainty is political. Mandates shift, coalitions wobble, elections loom. Not all states are Lannisters.

Revenue, reserves, and growth potential will always set the baseline. But how markets understand and price the politics of repayment — that’s the part we care about. In the last post, I looked at the international and domestic institutions that help build sovereign credibility. Here, we dive into one of the longest-running debates in the political economy of state finance: does democracy pay?

It’s a question with inevitable urgency in an era of democratic backsliding and regime uncertainty.

The Democratic Advantage

For a long stretch after the Cold War, scholars were convinced that democracy came with a built‑in edge. The logic was consistent and the findings stacked up across subfields. Inclusive government lead to democracies fighting wars more effectively and avoiding fighting each other; cooperating more easily through institutions; using economic carrots and sticks more successfully; and democracies delivered material benefits at home, from human capital to growth. If world politics was an evolutionary contest, the empirics were backing up the notion that liberal democracy was the dominant strategy.

The core mechanism behind these findings was about checks and balances accompanied by the promise of accountability, and it was quickly extended to the credit markets. The classic statement came from Schultz and Weingast. Money is the sinews of power, and the states that win long-run geopolitical competitions are the ones that can borrow cheaply and persistently. Representative institutions, they argue, provide exactly that edge.

By constraining rulers through parliaments, courts, and regular elections, democracies give creditors a way to punish default—politically, not just economically. That makes promises to repay more credible. In their historical comparisons — Britain versus France from the late seventeenth century, the United States versus the Soviet Union during the Cold War — the liberal state repeatedly out-financed its rivals. Easy access to credit enabled tax smoothing, letting governments borrow during crises rather than impose politically explosive taxes. Over decades, that financial flexibility compounded into military and economic dominance.

This logic carried enormous weight. It linked domestic institutions to international power through a clean causal chain:

constraints → credibility → credit → endurance.

But once scholars moved from long-run history to contemporary developing economies, cracks appeared quickly.

Saiegh’s initial intervention was blunt. Using cross-national data on debt rescheduling and interest rates, he showed that democracies in the developing world are actually more likely to reschedule their debt—and that interest rates don’t systematically differ between democracies and autocracies once risk is priced in. The core assumption doing the work in Schultz and Weingast — that creditors are embedded domestic actors who can punish sovereigns — often just doesn’t hold in poorer countries. Foreign lenders aren’t voters.

By contrast, the median voters doesn't hold large savings. And multilateral lenders muddy the picture further by providing concessional finance precisely when private markets pull back. In that world, regime type shows up in default behavior, not pricing—and even there, not in the direction democratic-advantage theorists would expect.

A similar conclusion emerged in broader analyses of credit ratings. Using panel data and interviews with analysts at Moody’s, S&P, and Fitch, political regime type appeared to have little independent effect on sovereign ratings for developing countries. Ratings moved with trade exposure, inflation, growth, and — least surprisingly — past default. Economics trumps democracy.

At this point, the democratic advantage looked to have been lost to history.

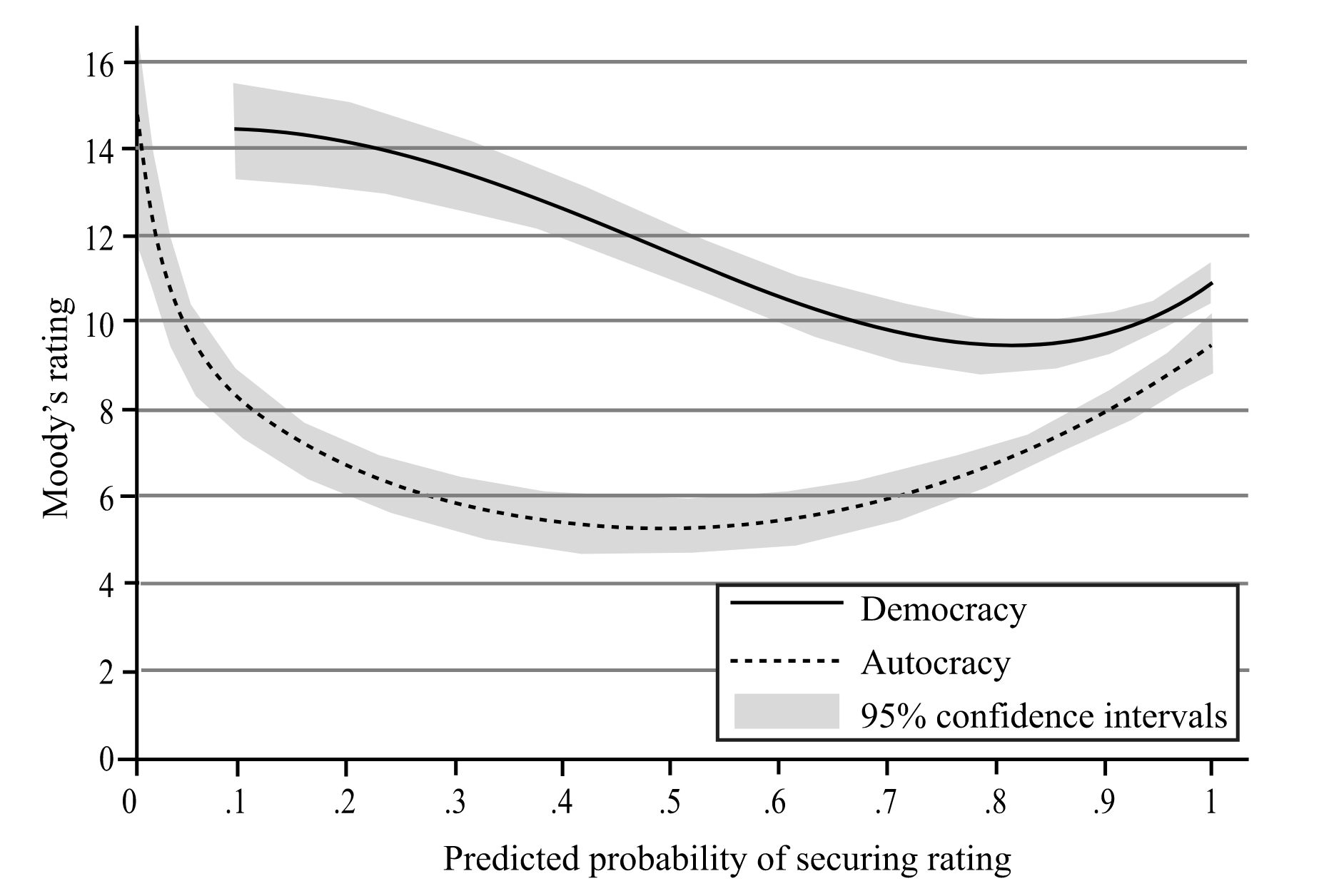

But Beaulieu, Cox, and Saiegh argue that it was hiding in plain sight - as a function of selection effects. During the '80s and '90s, the data period that most earlier studies analyzed, most autocracies never even entered the bond market, let alone bothered to receive ratings. Treating ratings as the outcome ignores the more fundamental gatekeeping role of access.

The scholars model this explicitly using a “reservation rating” framework. Governments seek ratings only if they expect to clear a minimum acceptable threshold - democracies, they show, were roughly four times more likely to be rated at all. Once you correct for that selection and treat GDP per capita as endogenous to political institutions, a democratic advantage reappears—twofold, in fact. Democracies gain access more easily, and conditional on access, receive better ratings.

This reframes the debate. The advantage isn’t necessarily cheaper borrowing given a bond issue; it’s the ability to borrow in the first place.

Finally, more recent work flips the question from levels to erosion. Yoo asks what happens when democracies backslide. Using V-Dem’s Episodes of Regime Transformation dataset and matching techniques to address endogeneity, he shows that democratic erosion is systematically associated with rating downgrades. Markets don’t just care about whether elections exist. They do appear to care about whether constraints are weakening. Backsliding undermines the very commitment mechanisms that earlier theories highlighted.

Which parts of democracy matter?

Democracy is a broad term. It gets regularly bastardized. The work above was pointing to a bunch of different features that might matter to investors - Elections? Voters? Courts? Elites? Or maybe it was just the bias of rich investors residing in democracies?

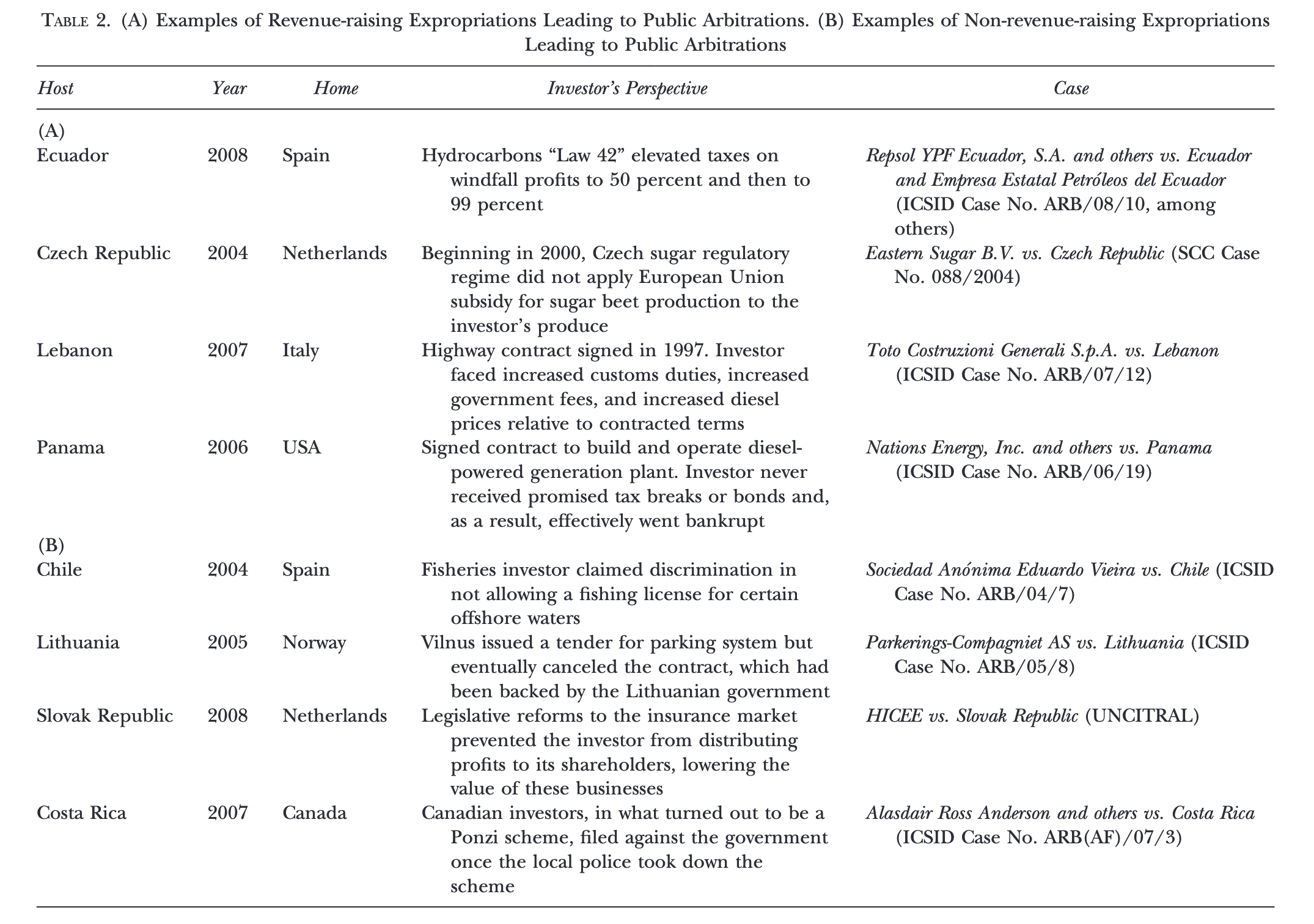

One of the cleanest demonstrations that “good institutions” don’t map neatly onto sovereign credit markets comes from Wellhausen’s work on expropriation. She starts with a deliberately provocative question:

if a government seizes a multinational corporation’s assets, does a hedge fund care?

Using data on 237 public investment arbitrations across 32 countries between 1995 and 2011, Wellhausen distinguishes between expropriations that generate revenue for the state and those that do not. The intuition is straightforward. Bondholders care about debt serviceability, not investor rights per se, going back to the economics acting as the baseline. If an expropriation transfers assets from a firm to the state and improves the government’s fiscal position, that can reduce perceived default risk—even if it violates property rights and triggers international arbitration.

Money can compensate for institutions.

Methodologically, she links arbitration events to long-run sovereign bond spreads and shows a sharp divergence:

Non-revenue-raising expropriations followed by arbitration are punished by markets.

Revenue-raising expropriations are associated with lower borrowing costs.

This is a devastating blow to the idea that respect for property rights—or liberal legality more broadly—is automatically rewarded in sovereign debt markets.

Bondholders align with investors when expropriation hurts the balance sheet. They defect when it helps.

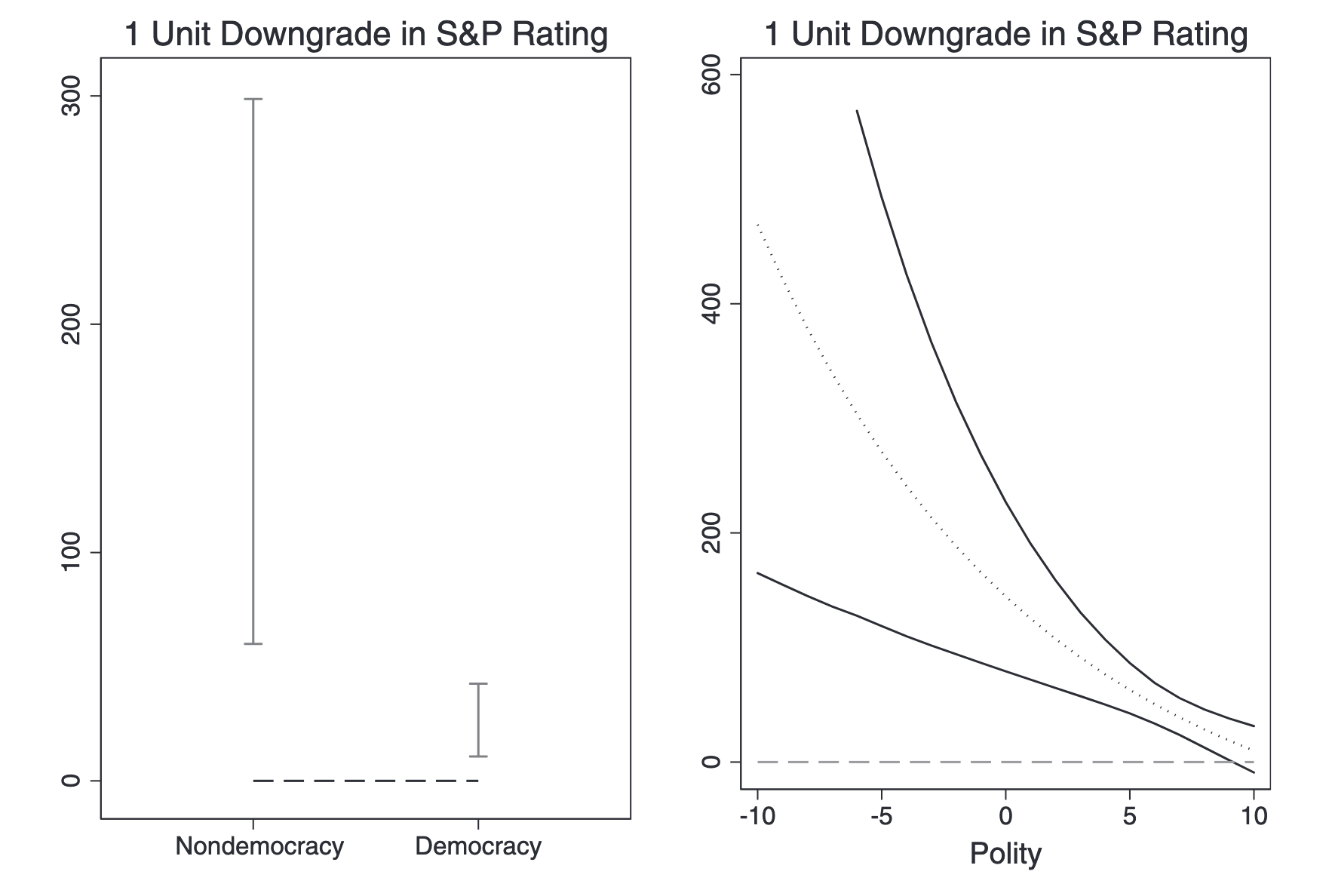

Another core pillar of the democratic advantage is electoral accountability. Voters punish leaders who default, making repayment more credible. DiGiuseppe and Shea take this mechanism seriously, but flip it.

Using event history analysis of leader survival across regime types, they examine who actually suffers politically when credit dries up. Their data link changes in sovereign credit ratings and bond spreads to the hazard of leaders losing office, distinguishing democracies from nondemocracies.

The top line takeaway undercuts the logic of the democratic advantage. Credit downgrades hurt nondemocratic leaders far more than democratic ones. A one-unit downgrade increases the hazard of removal by roughly. 30% in democracies. The risk of losing office jumpts to 155% in nondemocracies

Again the scholars rely on selectorate theory. Autocrats rely on credit to fund private goods for a small winning coalition. When credit tightens, loyalty collapses quickly. Democratic leaders, by contrast, rely more on public goods, and credit shocks don’t destabilize their coalitions to the same degree.

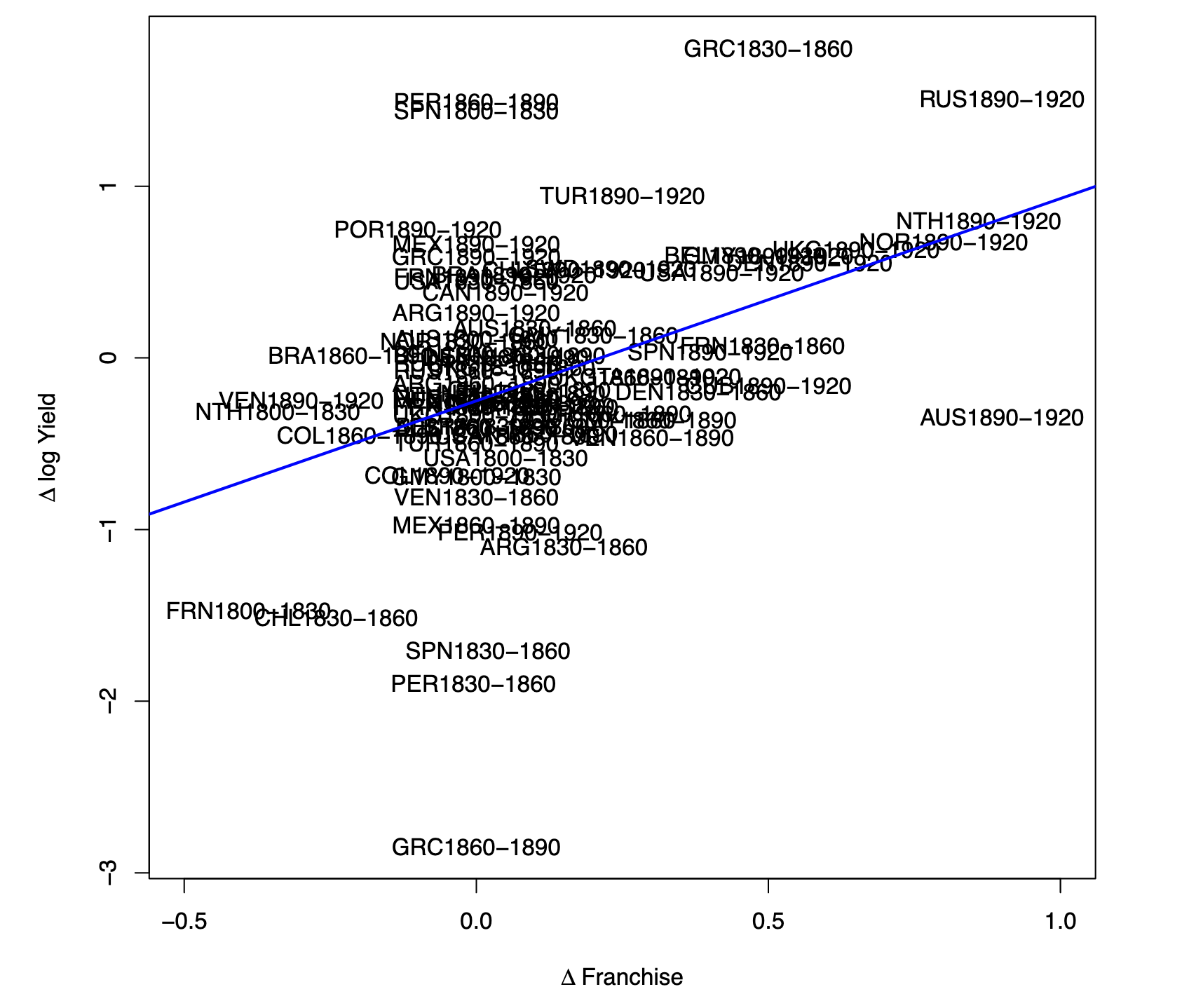

If democracy were intrinsically reassuring to investors, expanding it should always lower risk. Dasgupta and Ziblatt show that historically, it often did the opposite.

They assemble a remarkable dataset covering franchise extensions and long-term sovereign bond yields across 26 countries between 1800 and 1920. Exploiting the staggered timing of voting reforms in a fixed-effects panel, they show that major expansions of the franchise were followed by large and persistent increases in sovereign yields.

The effects are not anticipatory. Yields are flat before reforms, rise sharply around the reform window, and remain elevated for decades. Early franchise extensions—when inequality was highest—produced the largest spikes in risk premia.

Here the logic of democracy is again flipped from the work referenced in the previous section. Extending the vote shifted power away from financial elites who cared deeply about repayment toward poorer voters who were more tolerant of default and redistribution. Importantly, this occurs after parliamentary constraints already existed. Extending participation is not the same thing as constraining the executive.

The democratic advantage, in other words, was never about democracy per se. It was about who democracy empowered.

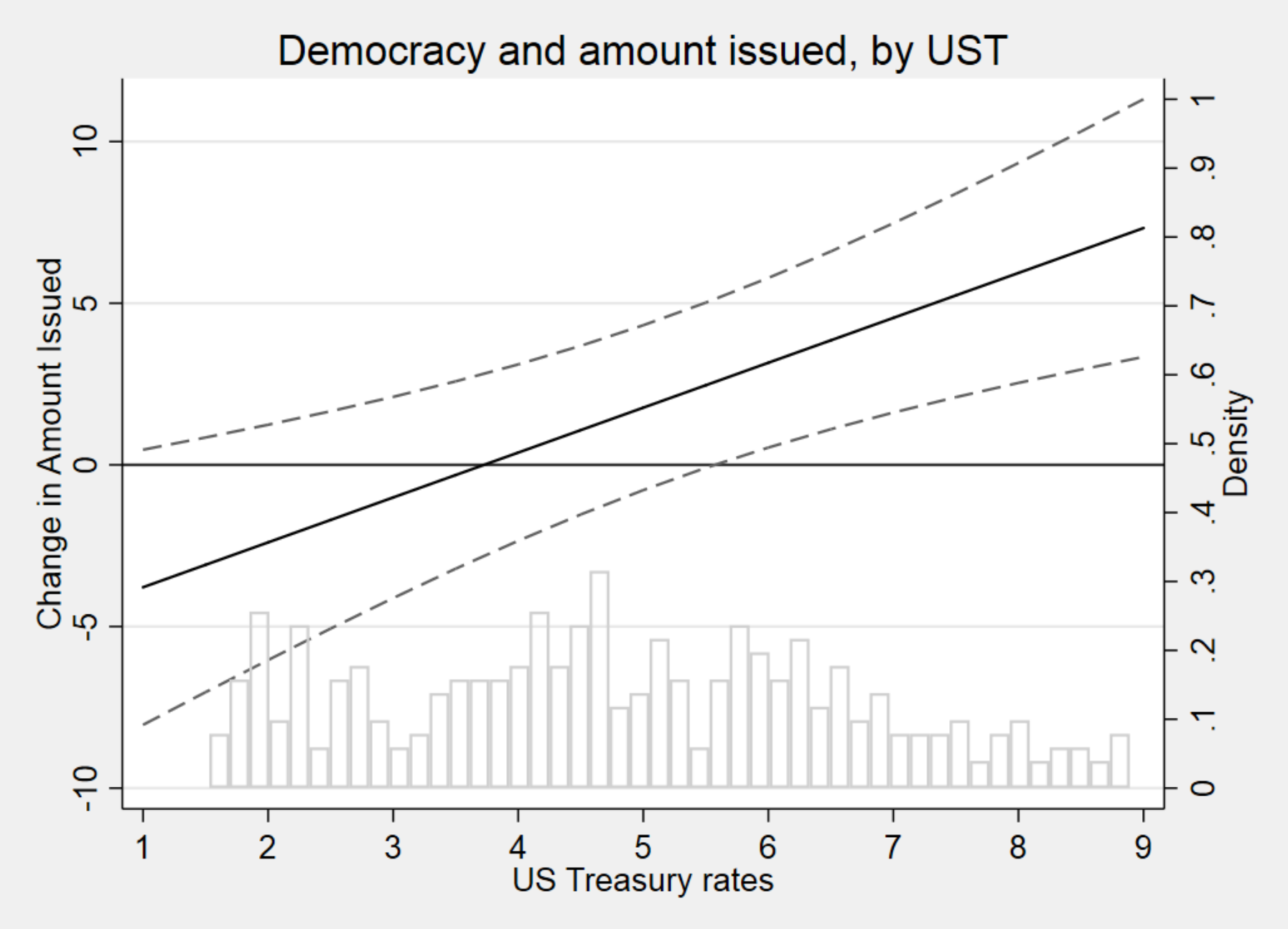

The scholarship thus far has largely looked at countries in isolation. but borrowing always happens in an international environment - sometimes, low rates in the US incentivize investors go "search for yield" but when liquidity is low they can get decent returns by just investing in the safe asset.

Using data on roughly 245,000 bond issues from 131 countries between 1990 and 2016, Ballard-Rosa et al. model issuance probabilities as a function of domestic institutions and global liquidity. Democracy, executive constraints, and transparency matter only when investors are risk-averse.

When global interest rates are low and capital is abundant, political institutions barely register. When liquidity tightens, those same institutions suddenly become relevant.

Methodologically, this is a rare paper that explicitly models access, not just pricing, and interacts domestic politics with U.S. Treasury rates to capture shifts in global risk appetite.

This reframes the democratic advantage as episodic, not structural, or in the words of the authors, "contingent." Institutions matter only when markets are looking for reasons to say no.

Is democratic gain actually about gains in transparency?

By now, it should be clear that “democracy” is doing a lot of conceptual work. Elections don’t consistently discipline repayment. Franchise expansion can raise borrowing costs. Property rights only matter when they affect the balance sheet. And institutional constraints only bite when global liquidity dries up.

What does survive across these studies is something narrower and more concrete. Much like the rest of the markets, sovereign debt is about (access to) information.

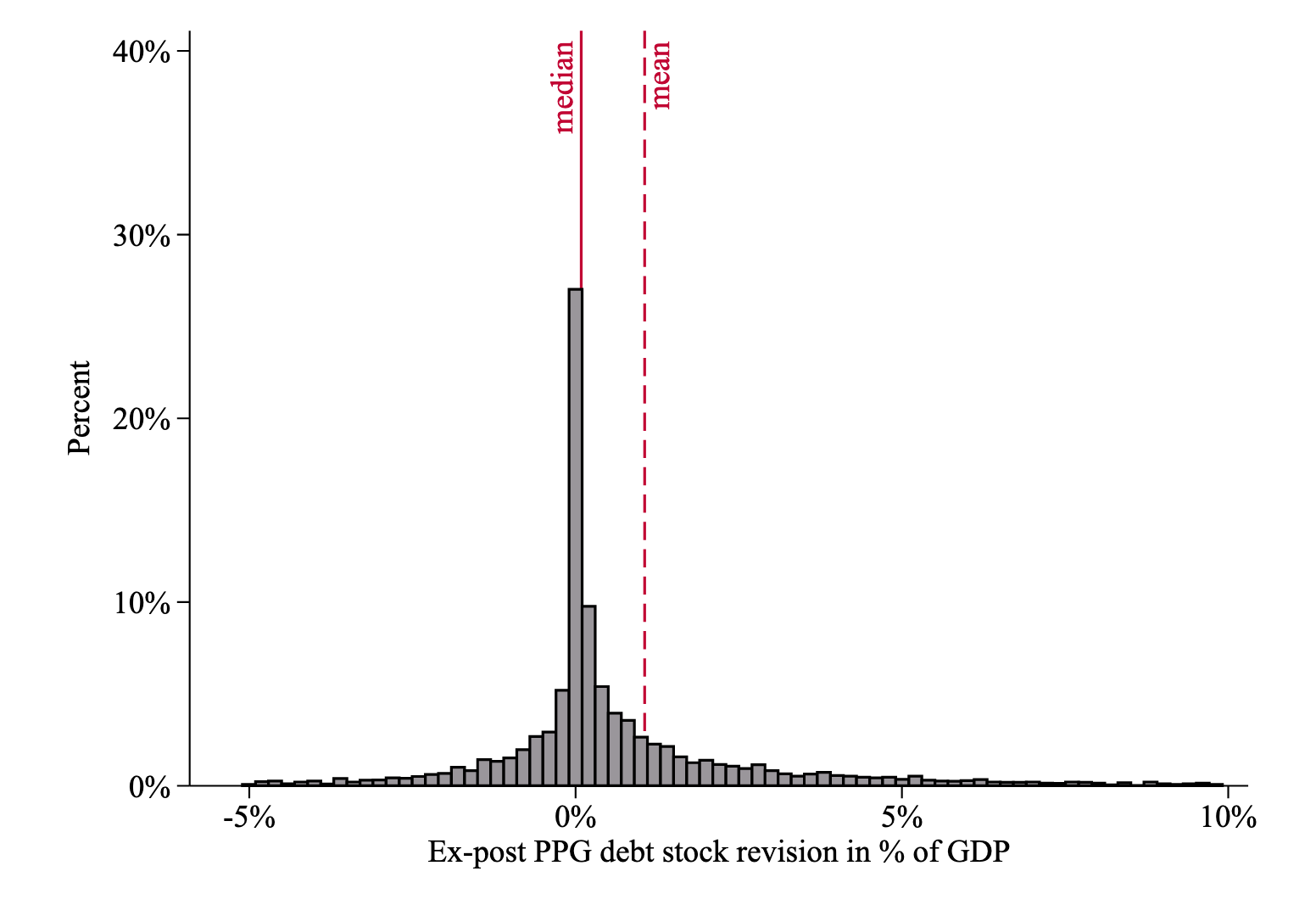

The most direct evidence comes from work on hidden debt. Using a remarkable dataset of more than 50 vintages of World Bank debt statistics, covering 146 countries over five decades, Horn et al. track how reported debt figures are revised over time. The findings are damning. Debt is systematically underreported, by roughly 1% of GDP on average, across regions and income levels. Hidden debt accumulates during boom years and is revealed during busts.

Those busts, and revisions, are often accompanied by IMF programs or outright defaults. And when restructuring occurs, higher hidden debt is associated with larger creditor losses.

This is powerful analysis precisely because it sidesteps intent. Instead of asking whether governments lie, the paper observes when the truth eventually comes out.

Hidden debt is most prevalent in countries with weaker institutions and is especially severe for bilateral and non-bond commercial lending. Stuff like borrowing from China. Those are the kinds of liabilities that have grown over the last two decades in the backdrop of a booming bond market. Opacity is not noise. It is a structural feature of modern sovereign finance.

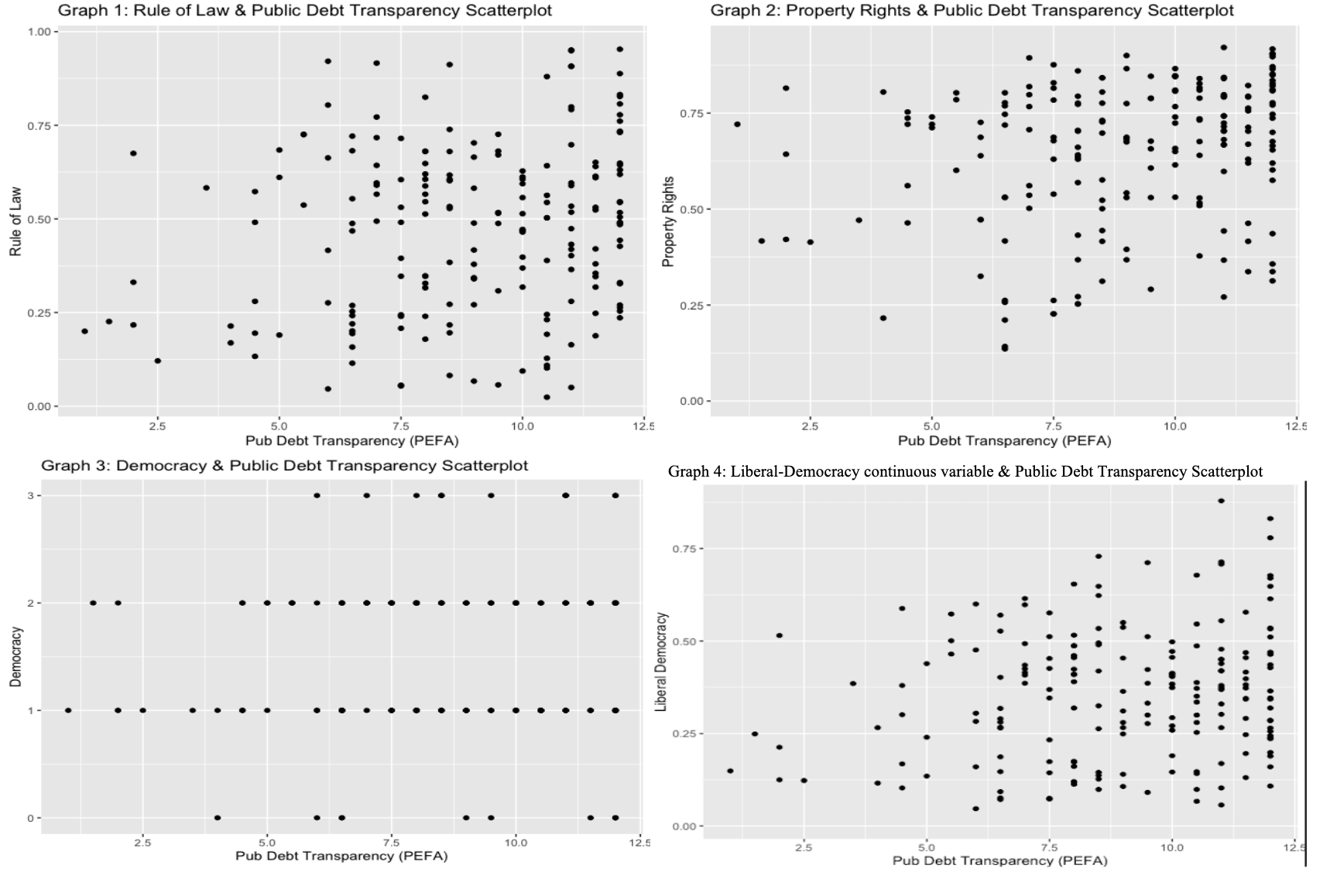

Rather than treating transparency as a diffuse governance virtue, Cormier isolates public debt transparency itself. Using data from the Public Expenditure and Financial Accountability (PEFA) assessments — which explicitly code debt reporting practices, audit procedures, and forward-looking debt strategies — he shows that countries with more transparent debt practices are more creditworthy, even after controlling for macro fundamentals.

The data cover 63 developing countries between 2005 and 2016. Crucially, when public debt transparency is included in the models, classic democratic-advantage variables — regime type, rule of law, property rights — largely lose significance.

The implication is uncomfortable but clean. Markets reward disclosure over democracy. And there’s no a priori reason that disclosure should be monopolized by democratic regimes, especially outside the OECD.

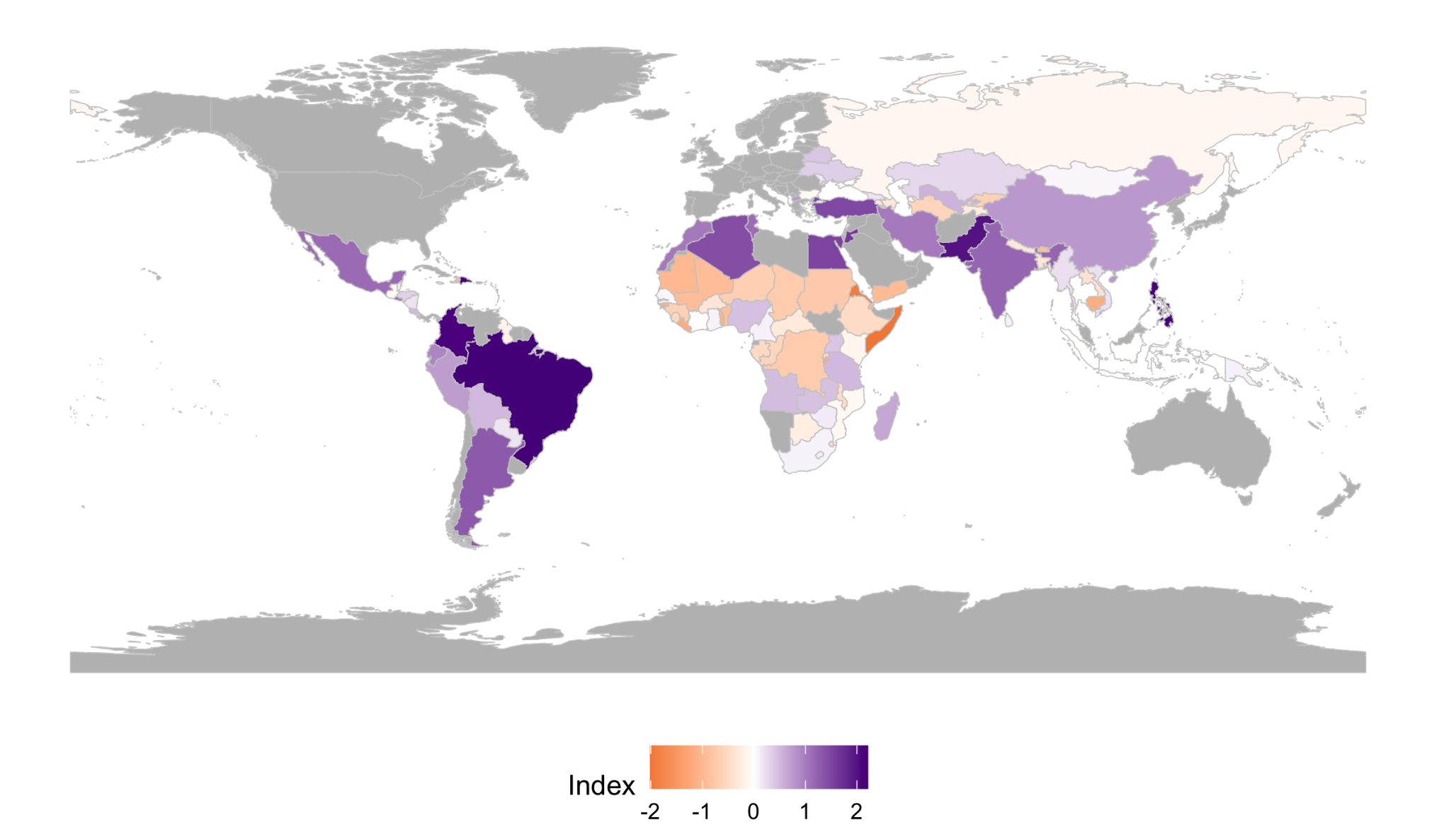

Bau et al. push this logic further by showing that transparency is not just a capacity constraint. They illustrate that it’s a political choice, tracking a range of important work in IR over the last few years. The scholars introduce the Princeton-NYU Debt Transparency Index (PNDT), constructed using Bayesian item response theory on missing data from the World Bank’s Debtor Reporting System. The index covers 113 countries from 1994 to 2022 and captures governments’ willingness to report debt data credibly and consistently.

Two results stand out. First, debt transparency varies enormously across countries and over time even within regime types.

Second, transparency declines around regular elections. Using variation in electoral timing, the authors show that governments systematically withhold debt information during scheduled elections — not irregular ones — suggesting deliberate concealment rather than bureaucratic overload. Democracy, in other words, can reduce transparency precisely when political incentives to hide liabilities are strongest.

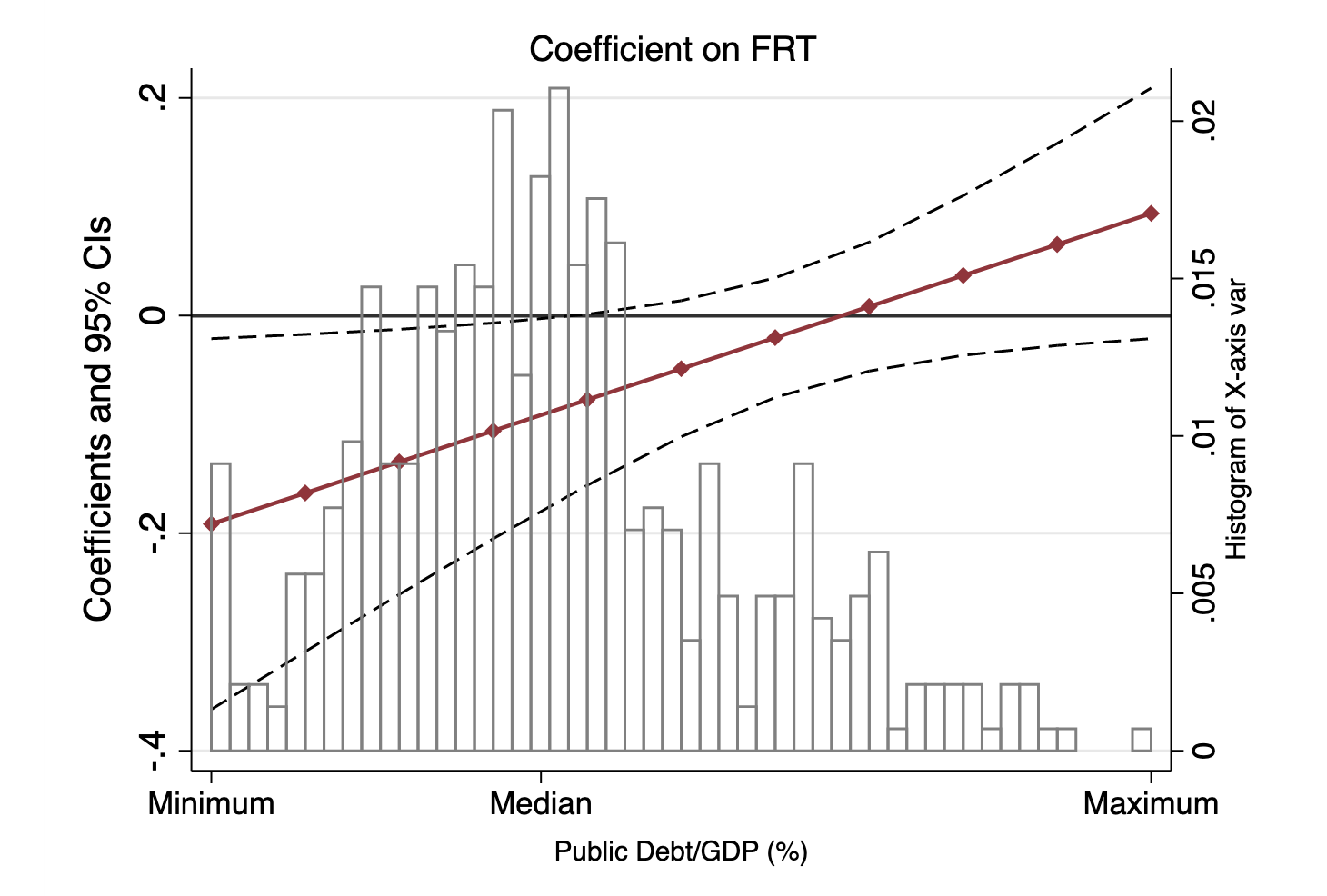

Finally, Copelovitch et al. extend the transparency argument beyond public debt to the private financial sector, where implicit liabilities often lurk. They construct a Financial Data Transparency (FDT) index based on governments’ reporting to the World Bank’s Global Financial Development Database, covering 69 countries from 1990 to 2013.

Their core finding is conditional. Transparency lowers borrowing costs, but only when public debt is relatively low. When debt levels are already high, disclosure no longer reassures investors; the bad news simply confirms their fears.

Across these papers, a consistent picture emerges. The democratic advantage isn’t about voters punishing default or institutions constraining executives in the abstract. It’s about whether investors can observe liabilities before they explode.

Democracy sometimes helps produce that visibility — through free media, reporting norms, and international scrutiny. But it can also undermine it, especially when electoral incentives favor concealment. What markets ultimately price is not regime type, but legibility.