Growth Models: The Need for, and Types of, Aggregate Demand

In Political Economy, growth is conventionally understood to be a function how workers are trained, how labor markets operate, and how firms finance themselves. Economic gains, from this vantage point, are largely a function of "supply-side" institutions. The policies that make firms more competitive or workers take on the skills that best fit national companies matter most.

Countries are then broken up into two main types: one withs the “liberal” institutions that foster innovation with flexible markets (like the U.S.) or “coordinated” systems that support incremental upgrades in manufacturing (like Germany). That's the TLDR version of a hugely influential body of work that goes under the Varieties of Capitalism (VoC) banner.

But when the financial crisis hit, and recovery remained elusive, the foundations of that framework began to crack. Why did countries with similar institutional structures perform so differently? And why did so many advanced economies, despite stable institutions, enter a long-run funk of low growth and rising inequality that was catchily titled "secular stagnation"?

The “Growth Models” perspective has recently emerged to answer those questions. Drawing on post-Keynesian macroeconomics, this framework asks a different set of questions. Firms matter, but who are they selling to? Institutions can lock in competitiveness, but how do they distribute wages, profits, and thereby purchasing power?

Basics of the Approach

The growth models perspective begins from a provocative, near century-old claim: modern capitalism is not driven primarily by efficiency or firm competitiveness, but by the search for demand. Without sufficient spending — by households, firms, governments, or foreign buyers - economic growth falters. When growth slows, so too does political stability.

There are two fundamental questions that drive the analysis: who is buying what? and with what money? The composition and source of demand - be it from wages, credit, investment, or exports — shapes how economies grow, and for how long. In the most recent wave of scholarship, the first writeres to really start asking these questions were Lucio Baccaro and Jonas Pontusson. Once they got working on the macro side, driven by some work on macro regimes, Baccaro, Mark Blyth, and Pontusson pulled together a monster volume of contributions spelling out what studying capitalism from the demand side should look like when global trade is integrated and capital is free to flow.

At the heart of this approach lies a post-Keynesian and Kaleckian inspired understanding of the macroeconomy. That means a few key assumptions. First, it starts from the premise that capital and labor are locked in a continual struggle over the gains from productivity. Economic output increases over time, but who benefits and how those gains are distributed determines future growth.

This is not a mere technical detail: when a greater share of income goes to labor (rather than profits), there is more consumption in an economy, because workers have a higher “marginal propensity to consume.” By definition, poorer people are more likely to spend any additional dollar they receive to buy stuff rather than stash it in the stock market. That means they spend(/consume) more of what they earn.

Together, these mechanisms produce a feedback loop:

rising wages → higher demand → greater firm investment to meet new demand → rising productivity.

That was the logic of the postwar wage-led growth that is often regarded as the golden age of capitalism despite capital being mostly locked inside national borders. This logic remains the theoretical foundation for the growth models approach. But we've been in an age of wage stagnation for basically 50 years, so countries needed to find new ways to grow.

From this vantage point, the income distribution is not just a moral or political issue. It’s an economic one. If too much income flows to the top, i.e., those who are less likely to spend it, demand falters. If productivity gains aren't distributed back into domestic wages (and instead remain with capital), economies must look elsewhere to sustain growth: through household debt, public transfers, or foreign buyers. But each of these substitutes brings its own fragilities.

The broader implication is that growth is not self-sustaining. There is no “natural” equilibrium to which economies revert. Instead, capitalism is an unstable system, constantly searching for new sources of demand, new political settlements, and new methods of accumulation.

That's why, for growth model analysts, aggregate demand matters more than institutional typologies or firm-level competitiveness. Countries grow not just because they become more efficient. They are ready to become more efficient because someone - somewhere - is spending. That demand can be internal (wage-led, investment-driven, state-backed) or external (export-led), but either way, its composition, sustainability, and political underpinnings are what matter most.

This helps explain a puzzle that other frameworks struggle with: why countries with similar institutions can experience very different growth trajectories, or why growth slows even when inflation is low, interest rates are near zero, and firms appear profitable. These are not anomalies. They are symptoms of a broader stagnationist tendency in advanced capitalism: one where existing sources of demand have weakened and no new engine has fully replaced them.

This also leads to a second, critical insight. Countries are not islands and neither are their growth models. Their growth models are shaped and constrained by their place in the global economy. Credit-financed consumption requires global capital inflows. Export-led models depend on trading partners with the willingness (and capacity) to consume.

In this sense, growth models are both domestic and international. They emerge from national political bargains—between labor and capital, or governments and firms. But they are only viable within broader global configurations of demand.

What is a growth model?

Ok now that we've got all that throat clearing out of the way, what exactly is a growth model? As Baccaro, Blyth and Pontusson (2022) put it, it's not a policy agenda or a temporary strategy. It's a stable set of macroeconomic patterns - a way that a country generates, channels, and sustains demand over time.

Some countries rely on wage growth and household consumption. Others suppress domestic demand and lean on exports. Some combine public investment with private borrowing. But in each case, the model must be politically maintained via coalitions, institutions, and ideologies that legitimize its distributional outcomes.

Models vs. Policy

It’s also important to distinguish between growth models from growth strategies. A strategy is what governments do. The policy roadmap to jumpstart or sustain growth, whether through tax cuts, infrastructure investment, or industrial subsidies. In contrast, a growth model is how an economy actually functions. It's how a country generates demand, distributes income, and channels investment over time regardless of whether the empirical reality aligns with policymaker intentions. It’s the underlying structure, not just the chosen tactics.

While strategies can be deliberate and short-term, growth models are deeper, slower-moving, and often path-dependent. The policy toolkit could be working to channel the growth model or to even undermine it, like when say a country that relies on consumption to grow redistributes wealth to the top through a tax cut...

Consumption-/Debt-Led Growth

I read Capitalizing on Crisis by Greta Krippner back in my undergrad years just when it was coming out, as the the aftermath of the global financial crisis was in full force. She examines how the American state managed to survive repeated legitimacy crises in the '70s and '80s as the costs of promising the American dream interacted with the hegemon's need to keep spending on defense, on the Vietnam War, on the Cold War.

Her answer was simple but fascinating to me at least - any time the US was facing growing societal backlash, it came up with a simple fix: let the people eat credit.

Krippner's logic becomes the premise for the first archetype of the GM approach:

When your economy relies on consumers buying stuff locally, and their wages aren't going up, lend them the money to keep up their purchasing power and you can keep the economy kicking along.

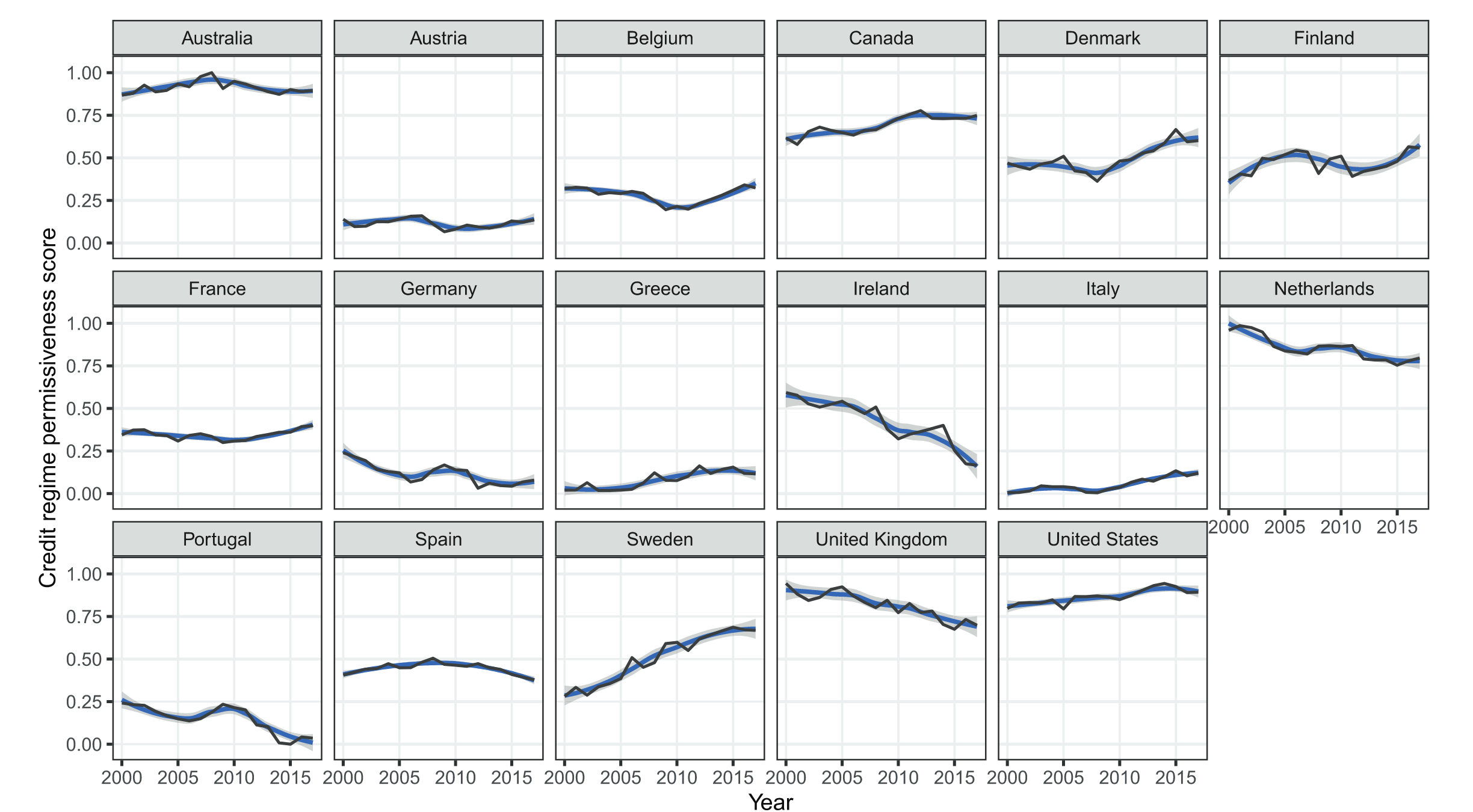

So in these systems, consumption isn’t primarily wage-driven. It’s debt-driven. While this was spelled out by a few different scholars initially, the most comprehensive description of the model comes from Alex Reisenbichler and Wiedemann. They point to two channels that have particularly helped substitute borrowing for wage growth: housing and personal debt.

1. The Housing Channel

The first, the housing channel, turns rising home prices into a broader macroeconomic stimulus. When property values go up, homeowners feel wealthier and spend more. What economists call a wealth effect. More importantly, rising home equity can be used as collateral to take out loans. Refinancing mortgages, borrowing against home equity, and expanding consumer credit, all have the net effect of increasing spending.

In other words, you take on leverage to buy your house - via a mortgage - but then the house lets you lever up even more.

This mechanism is especially powerful in asset-based welfare systems, where social spending is limited and wealth accumulation (usually via housing) plays an outsized role in ensuring security. In such regimes, housing markets become central to macroeconomic management. Rising home values are not just good news for individuals. They’re the engine of the national growth model.

2. The Income Maintenance Channel

But not everyone owns a home. So how do those without assets keep up? Households need to borrow to "smoot"h income losses when wages stagnate, jobs are lost, or living costs rise. This effect is again dramatic in countries with weak welfare states.

When the safety net frays, credit becomes a private substitute for public policy. Recent research shows that households borrow more when they live in places with stingier unemployment benefits. In the US, a 10-percentage-point drop in unemployment benefit generosity, for example, is associated with a 30% rise in household debt — about $5,300 on average.

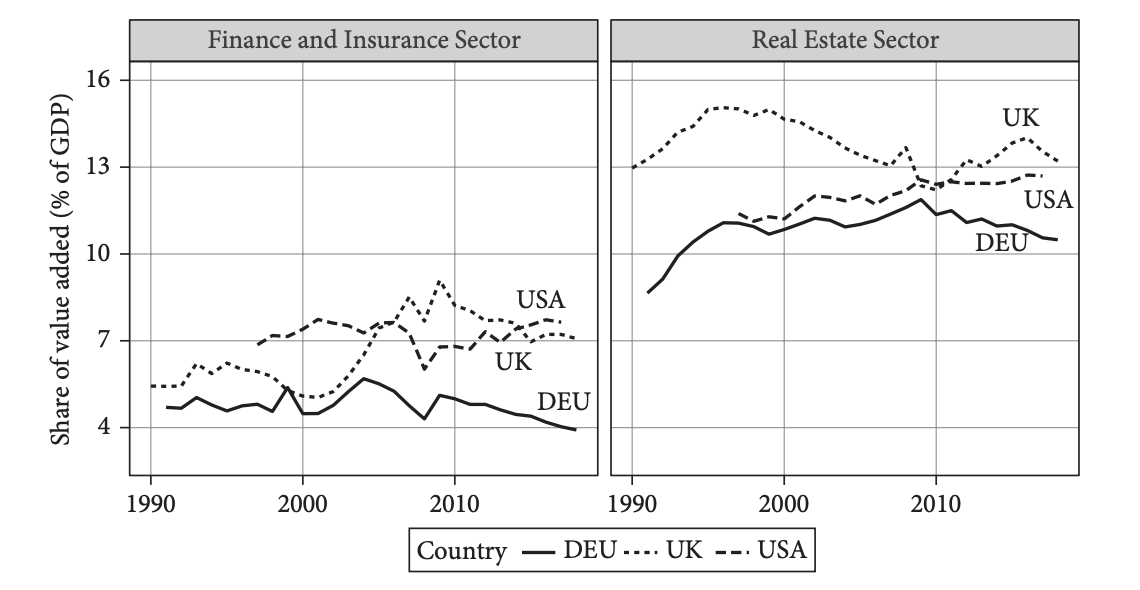

These credit channels are not just economic mechanisms. They’re inherently political. The FIRE sector (finance, insurance, and real estate) directly profits from growing debt and expanding asset values. But so do millions of homeowners who benefit from rising prices, tax breaks, and permissive lending rules. As a result, both center-left and center-right parties have converged around pro-credit policies, especially during economic downturns.

To put it simply, when labour doesn't have any power, borrowing replaces bargaining.

Asset Inflation as Growth Policy

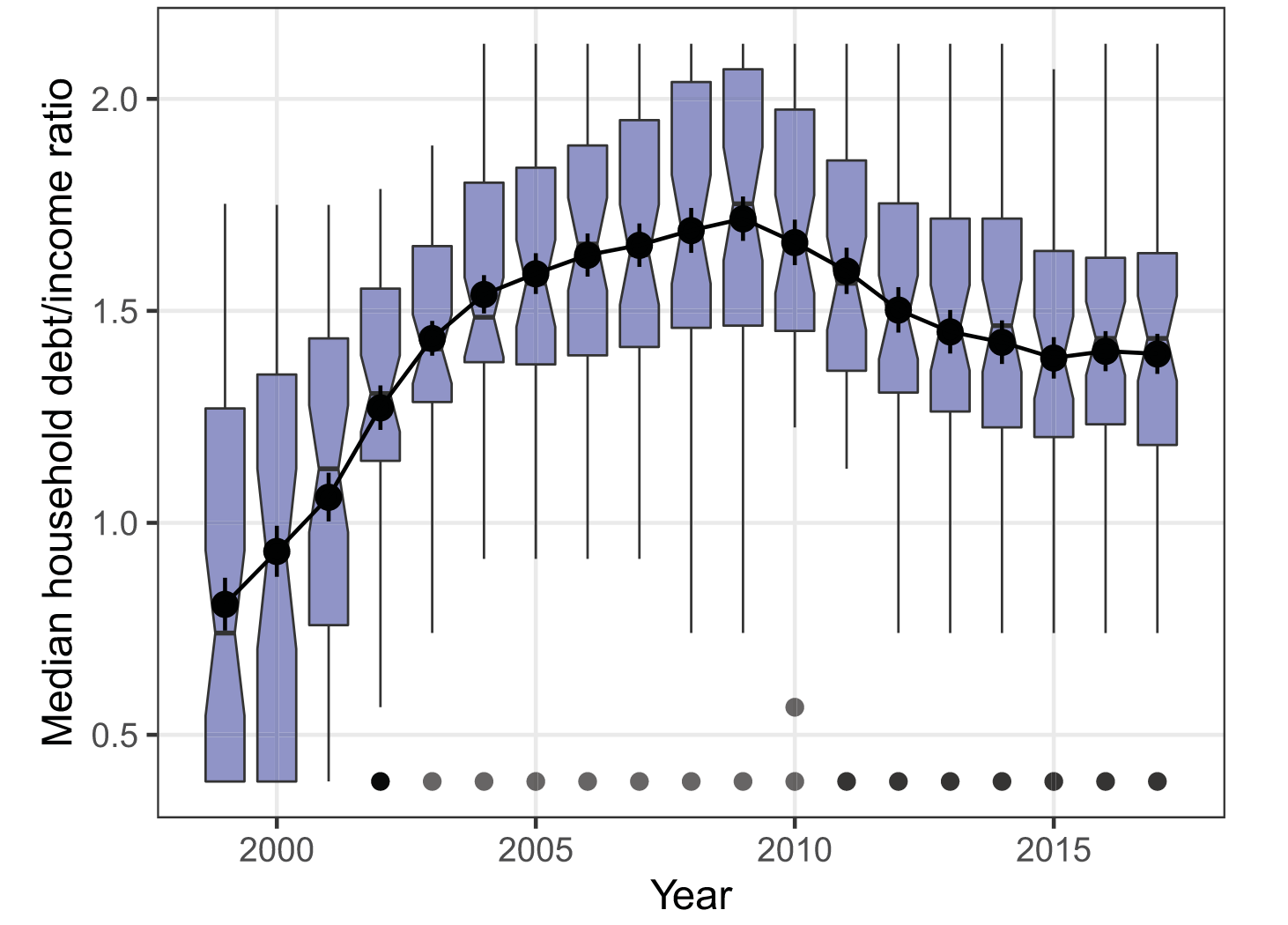

This growth model generates a highly unequal political economy. Existing asset owners win big, as their wealth increases and their ability to borrow expands. Those without assets must take on more debt just to maintain living standards. And as housing prices rise faster than wages, the ability to borrow becomes increasingly unequal.

Yet the consumption model can’t go on forever. Its core mechanism — asset inflation — is inherently unstable. Asset bubbles eventually burst, and debt burdens become unsustainable.

But not every crash happens the same way, at the same speed, or with the same effects. Your place in the financial hierarchy - how much other people want to hold your currency - conditions the sustainability. Some economies (like the US) can weather crashes by attracting foreign capital or running large deficits. Others, like Southern Europe or Turkey, have faced far more brutal corrections.

And rising indebtedness does appear make lose faith in the political establishment.

Still, many countries have tried their hand at consumption-led growth, from pre-2008 Spain and Ireland to Brazil and beyond. What distinguishes success or failure is not simply access to credit, but whether that access is politically and economically sustainable, and whether the growth it enables can survive rising debt, falling wages, or shifting global conditions.

The Export-Model

While debt-fueled consumption has driven growth in the Anglo-American world, an entirely different path has underpinned the economic success of countries like Germany, South Korea, and Japan. They sell stuff to other people engineering export-led growth. These models don’t rely on household borrowing to sustain demand. Instead, they suppress domestic consumption in order to boost price competitiveness abroad. The engine of growth is the rest of the world and the fuel is making their own citizens poorer.

At the heart of this strategy is a remarkably consistent set of policies: coordinated wage bargaining to keep labor costs low, conservative fiscal and monetary policy, strict housing credit regulation, and a relatively underdeveloped financial system that channels excess savings abroad. As Baccaro and Höpner (2022) note, these ingredients together create a powerful force of real undervaluation. The net goal is making sure domestic prices (inputs into the production process) rise more slowly than those of trading partners, making exports systematically cheaper.

This is not simply the result of market forces. It’s a set of political choices. German policymakers, for example, have long sought inflexible exchange rate regimes that translate domestic wage restraint into improved international competitiveness. From the gold standard to the euro, the goal has been to “lock in” relative prices and prevent currency appreciation that could undercut exporters.

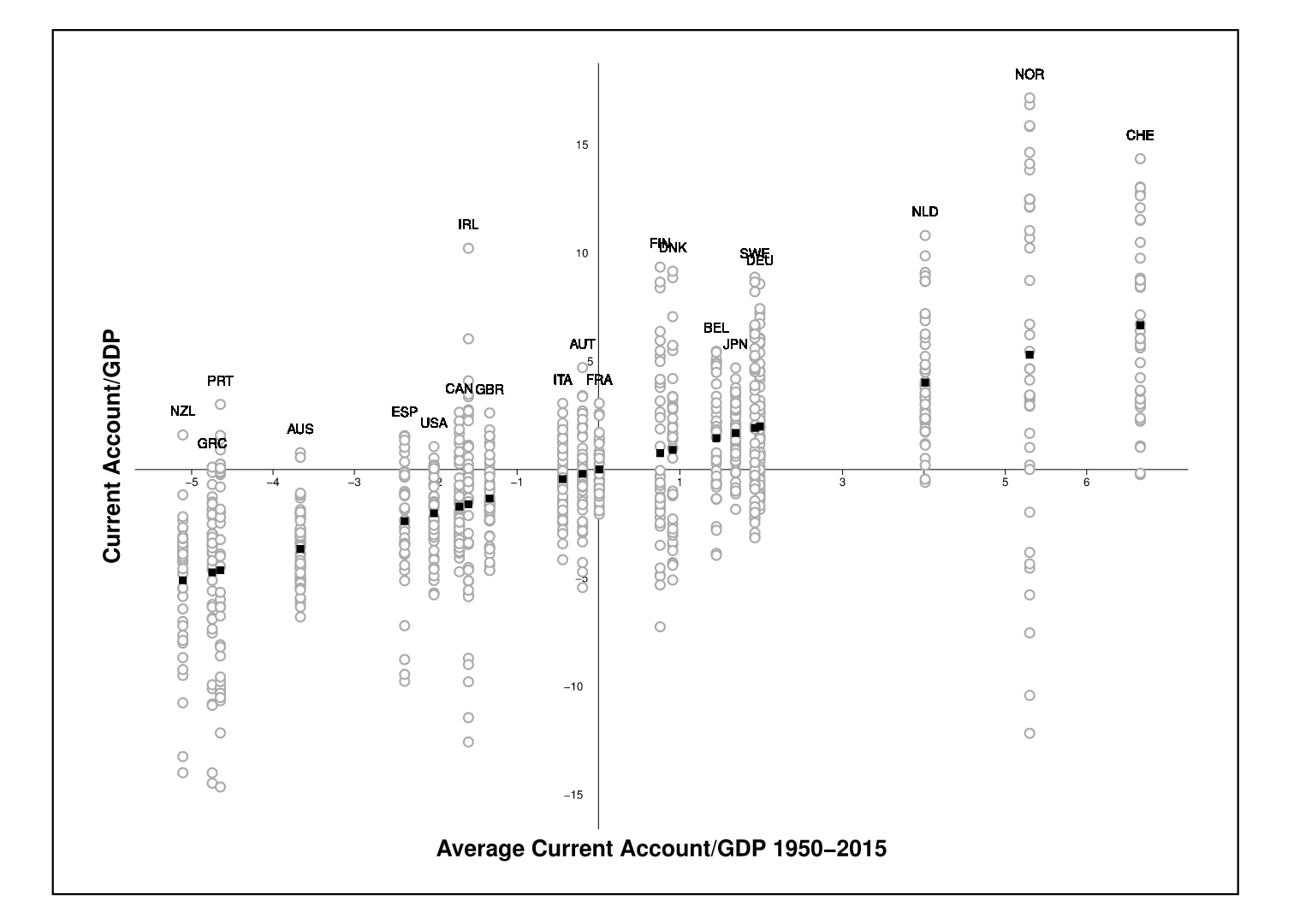

These surpluses are not just short-term phenomena as standard economic theory would expect. They reflect long-term institutional and political differences with labor markets playing a critical role. Manger and Sattler (2020) show that countries with highly coordinated wage bargaining systems (put simply, places with high union density) are far more likely to run surpluses than those with fragmented or individualized wage setting. In coordinated systems, export sectors enjoy stable, moderate wage growth, preserving price competitiveness and bolstering their political influence.

Focusing on OECD countries, they estimate that countries with the least coordinated systems consistently run current account deficits of about 2.5% of GDP, while the most coordinated systems generate surpluses around 3.4%.) And crucially, these patterns hold regardless of the exchange rate regime. Coordinated wage moderation alone can produce structural surpluses.

That is not to say exchange rates don't matter. In the case of the eurozone, Johnston and Matthijs (2022) argue that during the euro’s first decade, growth model diversity was tolerated. But after the debt crisis, the institutional reforms imposed by creditor countries (basically Germany) enshrined export-led strategies as the only acceptable path to growth. Fiscal rules were tightened, domestic demand was deprioritized, and structural reforms in the periphery were aimed at replicating German-style competitiveness.

The euro crisis was not just a monetary breakdown. It was a moment of the Germans enforcing what they think of as the optimal growth model. Their growth model. But if everyone is trying to export, who is going to buy anything?

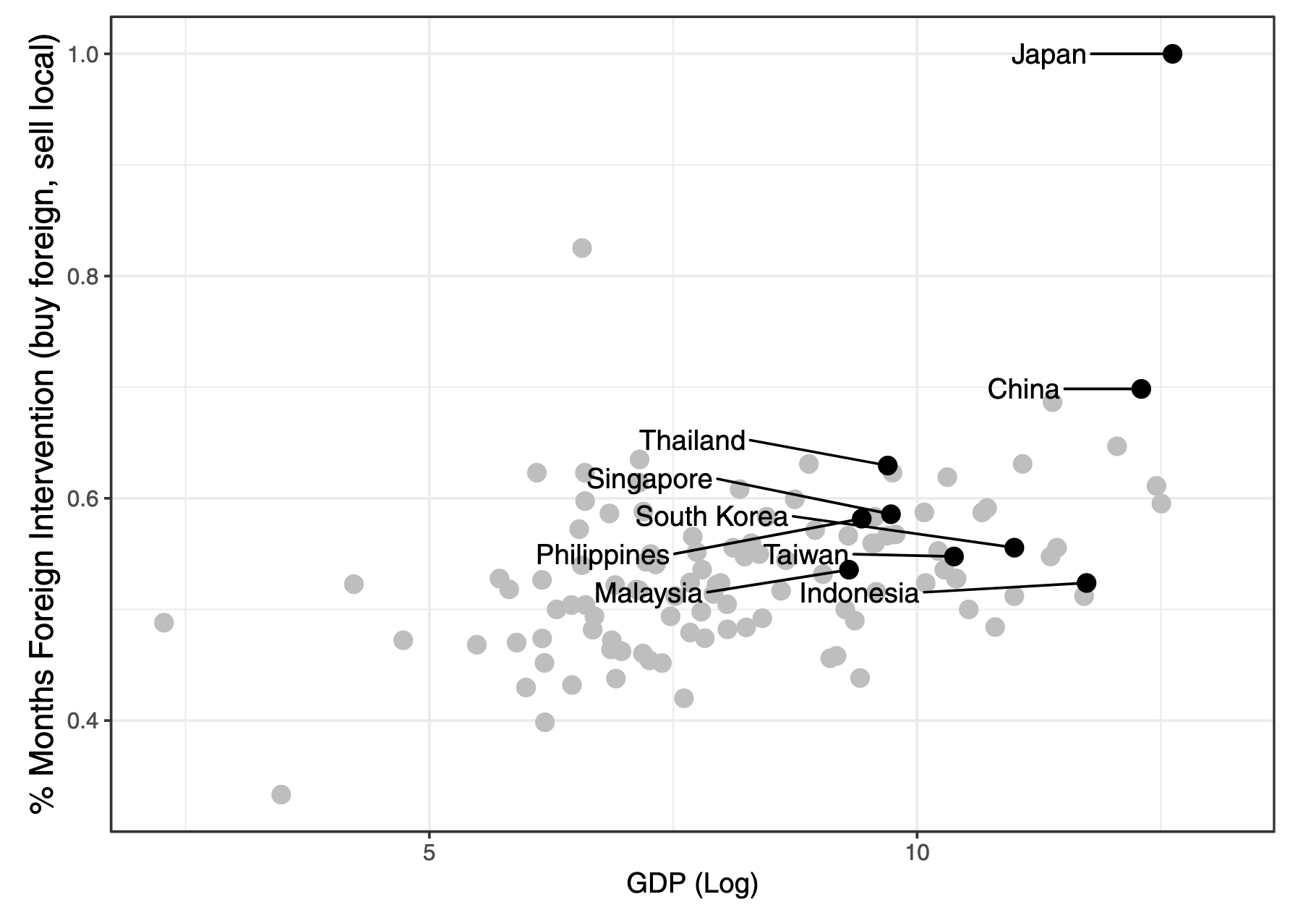

I am only loosely trying to pick on Germany. In East Asia, countries like Japan and South Korea have relied heavily on undervalued currencies to support export competitiveness. But rather than wage restraint, the key lever is often active intervention in the foreign exchange market. Manger and Nones (2025) use a novel method to track this. They apply machine learning to decades of financial newspaper articles in Japan and Korea to measure when exporters lobby for a weaker currency. The results show a strong link between these signals and subsequent government interventions to depreciate the exchange rate.

In both Europe and Asia, the export-led model relies on holding down domestic demand whether through wage restraint, tight housing credit, or limits on fiscal expansion. Investment flows abroad, domestic consumption is muted, and the health of the economy depends on demand elsewhere.

But this model is increasingly strained. As protectionism rises and geopolitical frictions mount, relying on foreign markets is no longer a safe bet. Eurozone surplus countries face pressure from the U.S. and developing economies alike. And in Asia, the politics of currency intervention grow more contested as citizens push back against stagnant wages and declining purchasing power.

The need for sub-national analysis

National growth models are effective descriptors but they also often miss what's happening under the hood. That's particularly true for many of the most successful economies of the past three decades that have managed to toggle different growth levers to ensure they keep growth constant rather than a function of forces outside their control.

China as a System of Systems

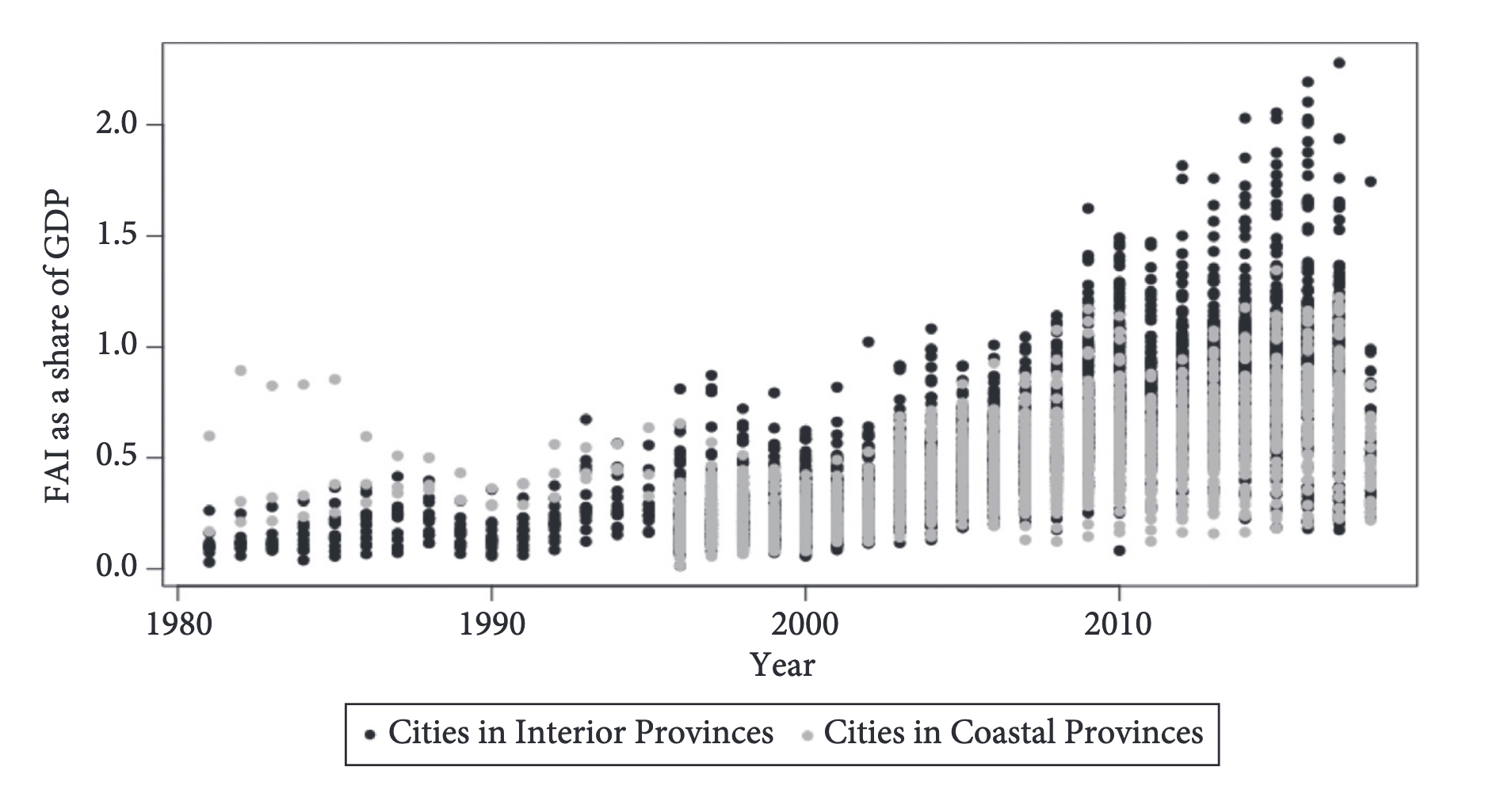

In public discourse, China has replaced Germany as the archetype of an export-led economy. But as Tan and Conran (2022) argue, this view is radically incomplete. China’s growth model is not singular. It is hybrid. And it is spatially organized.

For over four decades, China’s development has been shaped by two distinct, and at times contradictory, growth regimes:

A coastal export-led model rooted in foreign investment, supply chain integration, and manufacturing

An interior investment-led model built around state-owned enterprises (SOEs), infrastructure projects, and credit-fueled growth

These aren’t just geographic zones. They represent competing political coalitions and distributional logics within the Chinese party-state. They also reflect China’s attempt to balance external competitiveness with internal cohesion. To be globally integrated yet domestically stable.

This wasn't an accident but it also wasn't planned. China’s hybrid structure is the product of its incremental and experimental approach to reform after the Mao era.

Reforms were trialed through Special Economic Zones (SEZs) on the coast where liberalizing trade, reducing tariffs, and encouraging foreign direct investment. Inland China remained under a command economy, driven by state-directed investment, rural industrialization, and informal entrepreneurship.

This “dual track” system allowed market reforms to proceed without triggering national collapse, but also entrenched regionally specific growth logics that persist today.

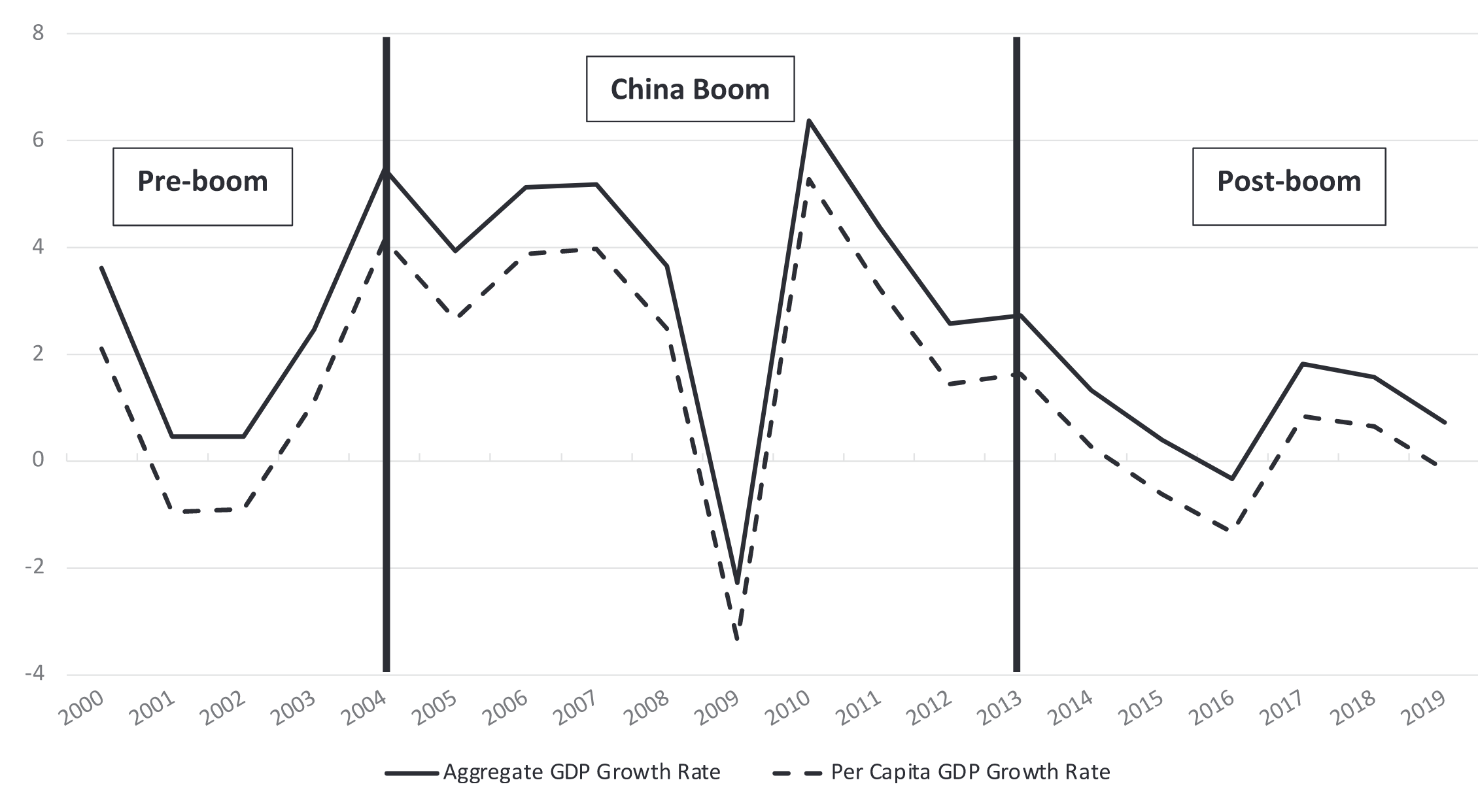

The balance between these two regimes usually shifts in response to global shocks. WTO entry in 2001 turbocharged the export-led model, especially in the Pearl River and Yangtze River Deltas. China became the “world’s factory.” The 2008 global financial crisis, however, exposed China’s vulnerability to external demand shocks. Exports collapsed, before they spent to save the global economy.

The Chinese state reverted to the investment-led model, unleashing a historic credit stimulus focused on infrastructure, housing, and SOEs in inland provinces. Growth was stabilized, but at a steep cpst. Debt surged, and overcapacity ballooned.

One common argument is that authoritarianism gives China the ability to shift between models as needed. There’s truth here: the 2008 stimulus, rapid SOE mobilization, and control over capital flows show the state’s capacity.

But Tan and Conran stress the limits to this flexibility. The political coalitions behind each model are entrenched — e.g. SOEs have powerful bureaucratic patrons. Rebalancing toward consumption-driven growth — a long-stated policy goal — has been repeatedly frustrated by these internal interests.

While China’s model may look cohesive from the outside, it’s riven by distributional conflicts and institutional inertia.

Understanding China as a "system of systems" reframes the debate around authoritarian capitalism. It also offers comparative insights:

Like the Eurozone, China contains regionally distinct growth regimes with uneven development, political tensions, and asymmetric adjustment.

China has been able to manage these tensions and channeled them towards recurrent growth. By contrast, countries can have sub-systems that consistently work against each other. This is clearest in Italy, which work on comparative capitalisms, has always struggled to categorize.

Italian Contradictions

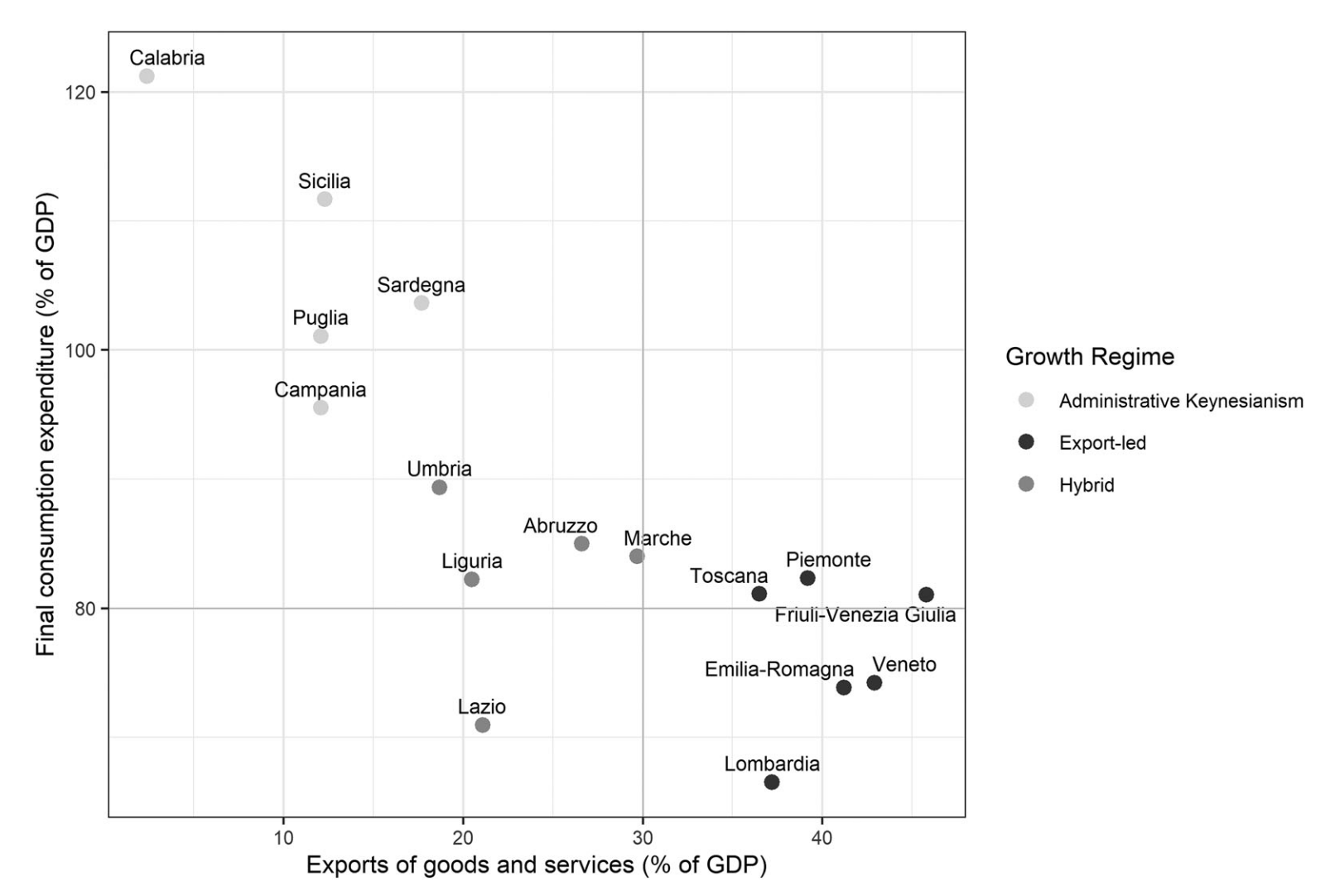

Di Carlo et al. (2024) illustrate that the country can only be understood as two distinct growth models and a common, iconic in the world of football, flag.

Northern Italy follows an export-led model, anchored in manufacturing, productivity, and territorial institutions that support international competitiveness.

Southern Italy operates under a model of administrative Keynesianism. Economic growth is driven by public employment, social transfers, and state forbearance on taxation and regulation.

These regimes do more than diverge economically. They underpin distinct political constituencies with competing preferences for fiscal policy, EU integration, and social protections.

This divergence explains why austerity policies after the Eurozone crisis hit the South far harder. Public wage freezes and fiscal cuts disproportionately hurt a region heavily reliant on state-driven demand. Meanwhile, the North’s export engine, more resilient and integrated into global trade, weathered the crisis more successfully. Crisis-response only furthered the country's internal divergence.

Less regions, more cities

But regional diversity isn’t just about lagging peripheries. Some growth models are hyper-concentrated engines of global accumulation. This is clearest when you we look at global financial centers like London or Amsterdam. Or more generally geographically concentrated countries like France and Ireland where a single city dominates GDP composition.

They are not just “parts” of national economies. They are functionally autonomous growth models embedded in transnational financial circuits and dependent more on global capital flows than on their national hinterlands.

As Fraccaroli et al. (2023) argue, these cities generate a disproportionate share of national GDP (Dublin: >50%, Amsterdam: ~33%, London: ~23%), while operating in niche positions within global financial markets.

They may thrive not just due to mobility of capital, but they do survive because of “place-specific social capital” and “linked professional ecologies.” That's a fancy way of saying people, and the interdependence of their success, matter.

How jobs relate to each other, how people working across different parts of an industry concentrate, can keep a growth model in-tact. Social, just as much as material ties, can bind. That explains why Brexit despite appearing an existential threat to the City of London has had relatively limited impacts. London’s “structural power” in the global financial architecture remained largely intact because the people working in industries matter.

This leads to a provocative claim. Many growth models are not national — they’re urban.

Adapting to the Global South

While growth model analysis emerged from the study of advanced capitalist economies, recent work has begun to adapt its insights to the Global South and semi-peripheral regions. These adaptations reflect not only variation in development paths, but also an alternate set of structural constraints shaped by global economic hierarchies, foreign capital, and balance-of-payments limitations.

Servicing Global Capital

In one strand of the literature, Bohle and Regan (2022) analyze how small states insert themselves into global economic networks by servicing the interests of global capital. Drawing on the framework developed by Schwartz and Blyth on types of interdependence, they show how countries like Ireland and Latvia have become crucial nodes in global wealth chains(GWCs) — circuits of capital that seek to avoid taxation, regulation, and accountability.

Ireland combines global value chains in tech and pharma with wealth chain infrastructure such as favorable tax regimes. Latvia, by contrast, developed as a financial entrepôt catering to Russian elites, branding itself the "Switzerland of the Baltics."

In both cases, the national growth model is shaped not primarily by domestic policy goals or macroeconomic paradigms, but by the needs and preferences of global firms and wealthy individuals. That does not mean all policy choices are driven by MNCs. Often they don't care about specific issues - they work in too many places - leaving plenty of room for smaller capital to politically operate.

FDI-Led Industrialization as the new Dependency

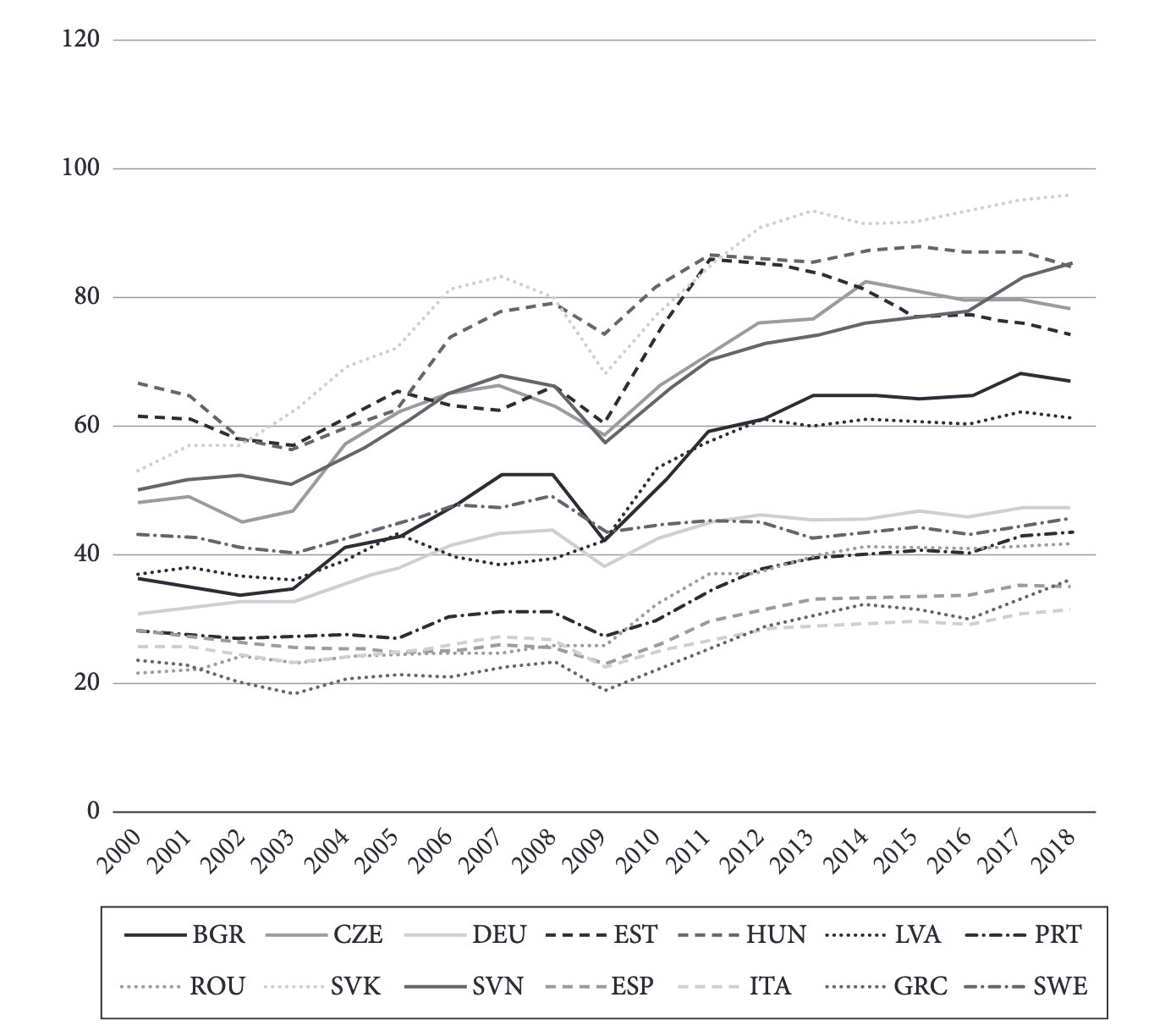

You can plug into global capital flows, or as many countries in Central and Eastern Europe (CEE) chose, you can find a spot in global trade. Countries like Hungary, Poland, Romania, and Slovakia have been deeply integrated into German-led manufacturing supply chains, offering cheap labor, deregulated labor markets, and low corporate taxes to attract investment. Remarkably they are even more export reliant than the German prototype.

As Ban and Adăscăliței (2022) argue, these economies function much like Mexico does to the US work as low-cost hubs within broader regional production networks. However, the model's success has triggered plenty of tensions with labor shortages and rising wages post-2008 squeezing profits.

Export dependence has deepened, while domestic demand remains fragile. Structural vulnerabilities persist in finance and banking, with foreign ownership amplifying exposure to global slowdowns.

These dependent growth models are inseparable from broader transformations in global capitalism like the rise of intangible capital and increasing financialization incentivizing offshoring of both capital and production.

As Bohle and Regan (2022) note, these arrangements may generate growth, but they also raise questions about the legitimacy and stability of domestic institutions, especially where they depend on flows of illicit or semi-legal wealth.

Constraints and Possibilities in the peripheries

The examples above largely adapt the Diminishing Returns toolkit, but recent work has been drawing attention to the limits of importing these models. Drawing on dependency theory and postcolonial IPE, scholars have emphasized:

- Developing countries always need to worry about having enough foreign currency to finance their imports and borrowing. Balance-of-payments (BoP) then acts as a central limitation on domestic-led growth.

- The frequency of economic crises triggered by problems outside their border - in the "core" - regularly undermines domestic growth coalitions

- Elites often use a wider range of strategies to make sure the growth model stays in check including patronage politics and outright repression, bringing with it a different set of political risk to stability as they often rely more on repression or clientelism than mass ideological consent

And the people backing the same model across countries often varies. As Kalanta (2024) and Spurga (2025) show in the Baltics, even within similar macro regimes, sectoral loci of growth and political are buttressed by different actors: Estonia built a service-based recovery after 2008, while Lithuania relied on low-wage manufacturing and wage restraint. That's true even when having to deal with internationally imposed policies.

These potential models all rely on the global economy, that are often subject to the preferences and choices of the global hegemons. Stallings (2025) offers a compelling IPE reinterpretation of Latin America’s recent growth history, arguing that the region’s post-1980s turn to export-led models was shaped by shifts in global demand. U.S.-oriented integration in Mexico, and commodity-fueled growth in South America, driven by China.

These growth paths created distinct winners and losers, with Mexico benefitting from sophisticated value chain integration (but limited regional development), while South America experienced reprimarization and renewed vulnerability to commodity price cycles.

Vulnerabilities

As Schedelik et al. (2024) put it, these economies frequently experience "stop-and-go growth patterns"—marked by sudden accelerations and equally dramatic collapses—due to their heightened exposure to global financial and trade shocks.

Peripheral growth models in ECEs[Emerging Capitalism Economies] can be expected to suffer from a relatively high degree of vulnerability… A large part of this vulnerability stems from the external sector… volatile export revenues [and] capital flows… have not yet been integrated into an encompassing theoretical framework of growth.

Domestic political-economic configurations mediate and (sometimes) mitigate these vulnerabilities, especially state-business.

Schedelik et al. (2024) synthesize this diversity by proposing a typology of peripheral growth models, each with distinct vulnerabilities:

| Growth Model | Driver | Vulnerability |

|---|---|---|

| Commodity-based export-led | Global prices | Dutch disease, deindustrialization |

| Debt-based consumption-led | Portfolio inflows | Sudden stops, financial crises |

| FDI-based investment-led | Multinational relocation | Middle-income trap, hollowing out |

So if there are so many problems associated with these models, such clear losers, why do they persist and what are the prospects for change? I cover that in the next post.