The (In)Stability of Growth Models

Rather than treating economic outcomes as purely the result of abstract market forces or static institutions, the Growth Model perspective emphasizes how countries generate and maintain aggregate demand — whether through exports, consumption, or investment — and how this process is shaped by political coalitions, domestic institutions, and international constraints.

At its core, a GM is defined by:

- The main driver of demand (e.g., net exports, household consumption),

- The distributional institutions that support this demand (such as wage bargaining systems, credit markets, and fiscal policy), and

- The international position of the country in global supply and financial chains.

Growth models vary across countries (and even within countries) but depend on each other — from Germany’s export-led strategy anchored in wage suppression and real undervaluation, to China’s investment-driven model, to Southern Europe’s pre-crisis consumption-led models fueled by credit expansion.

My previous post outlined the core features of these different models. One recurring theme is that they each generate substantial economic and, with that, political problems. So it begs the question, what sustains growth models in the face of mounting challenges?

Maintenance Mechanisms

Standard macroeconomic theory indicates that the prototypes of the Growth Model framework shouldn't be able to persist. An increase in exports should lead to currency appreciation and rising wages, which in turn erodes export competitiveness and rebalances trade, i.e., goods that are produced in a successful export economy become more expensive over time making room for other countries to take over their market share.

While this mechanism is observable in many economies, several others defy this logic. Economies like Germany, China, Singapore, and Taiwan maintain surpluses through deliberate maintenance mechanisms that suppress adjustment and reinforce the GM's core dynamics. If this sounds a lot to you like Trade Wars are Class Wars, you're right.

I discussed these in the previous post under maintenance channels in consumption regimes, and real undervaluation in export regimes. We can breakdown real undervaluation as a series of policies labelled "maintenance mechanisms", per Stephen Paduano, and they come in two broad varieties:

- Monetary maintenance: Foreign exchange intervention (often covert), reserve accumulation, and rechanneling of funds into sovereign wealth funds to neutralize currency appreciation pressures.

- Fiscal maintenance: Austerity, underinvestment in public services, and tax policies that suppress wages and consumption, thereby increasing private savings and external surpluses.

Historically, early-stage development has relied on unbalanced growth, privileging investment and exports over consumption. As Hirschman argued nearly 70 years back, this creates sectoral linkages that drive industrial transformation but also generate structural imbalances because of the active employment of maintenance mechanisms. Countries as different as the US, Japan, China, and Germany have followed some version of this export- and investment-led growth to upgrade their development status, breaking basics of economic theory in the process.

Even if countries want to switch, these growth patterns often result in long-term suppression of domestic demand. For instance, while consumption consistently accounts for nearly 70% of US GDP, it remains under 40% in China. Though consumption is growing in absolute terms, it plays a structurally smaller role in the macroeconomy.

Speculative Cycles and Finance-Led Growth

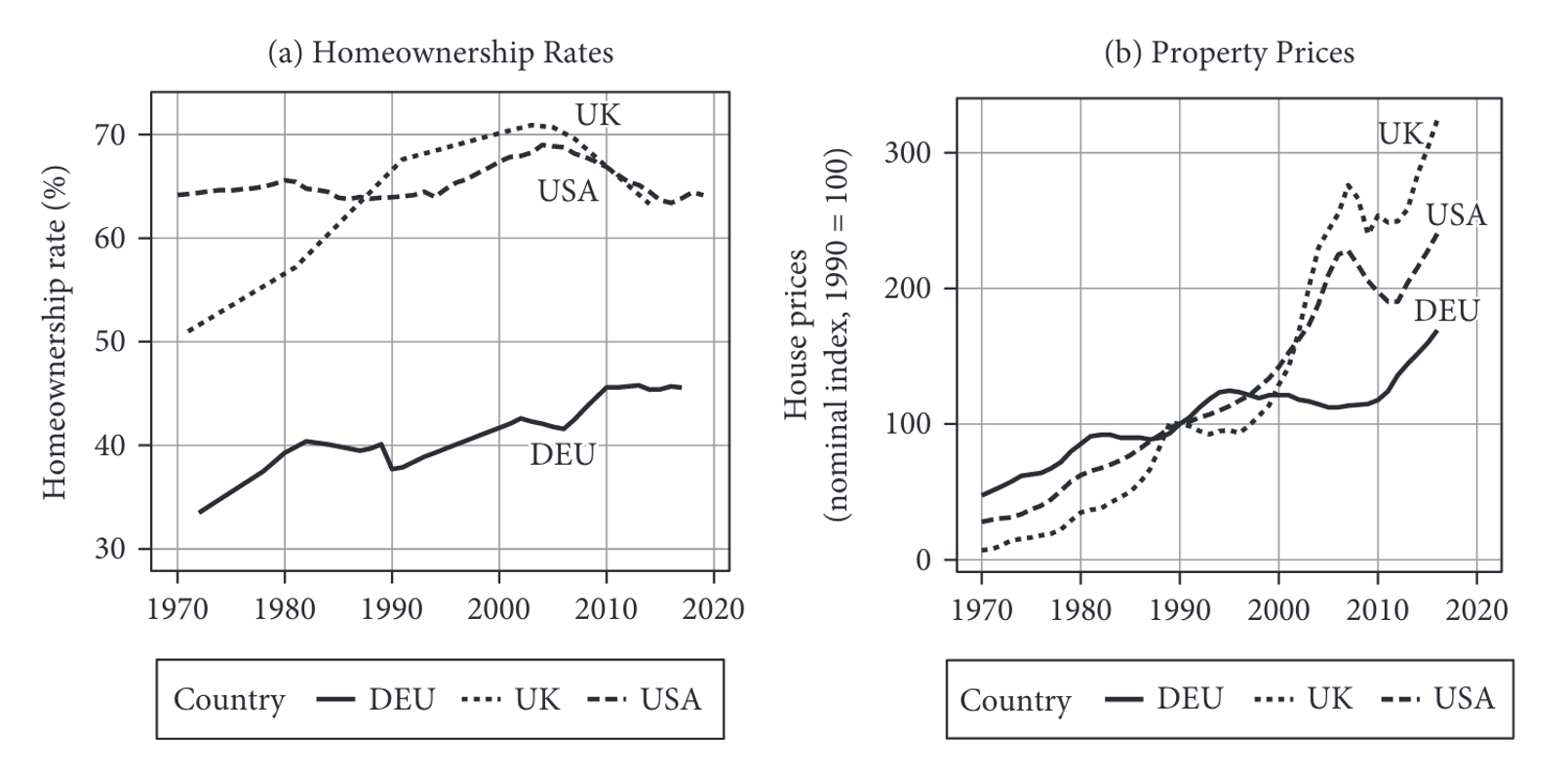

Not all growth models are built on external surpluses. In debt-led, consumption-driven GMs, such as those found in the US, UK, and parts of Southern Europe, demand is driven by private credit and asset price inflation, particularly in housing. As Reisenbichler and Wiediemann show, house prices in these contexts are central to the macroeconomics of growth. But Kohler et al. (2023) argue that even if rising home values stimulate consumption and residential investment, they also introduce Minskyan instability, as speculative cycles create boom-and-bust dynamics.

Crucially, the institutional structure of housing markets shapes how volatile these cycles become. Countries with high homeownership rates and liberal mortgage access — often encouraged by public policy — tend to experience more intense and frequent house price cycles. In these models, housing becomes a (speculative) growth driver, but also a key site of fragility.

Labor Markets and Welfare Institutions

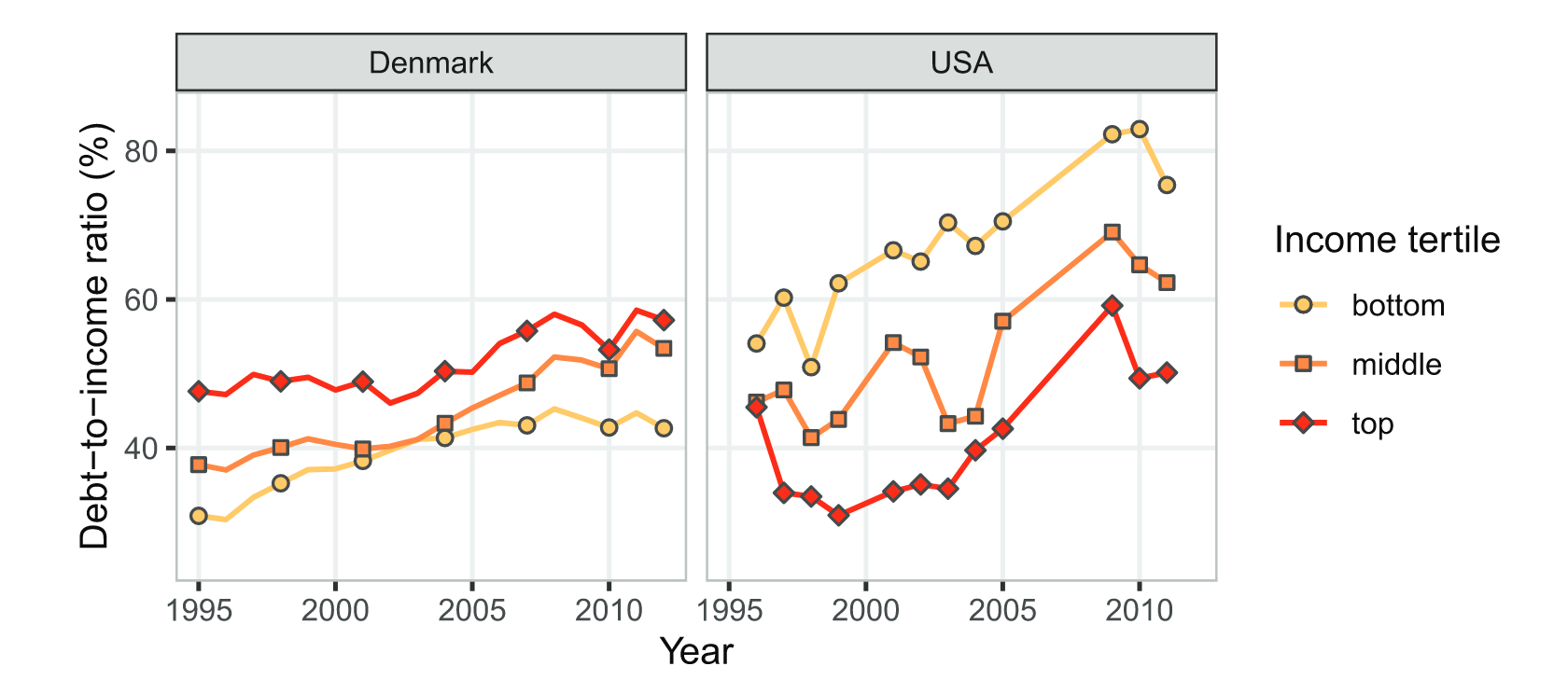

The GM perspective is not saying that policy-choices don't matter. It instead asks us to think through how they change aggregate demand. Welfare regimes, employment protection laws, and trade union density all influence the distribution of income, the structure of consumption, and thereby the resilience of demand. Scandinavian and Continental models — rooted in stronger labor protections and redistribution - tend to support more balanced demand regimes, while Anglo-liberal models rely more on credit-led consumption and exhibit higher levels of labor market flexibility.

These institutional variables are not merely auxiliary to GMs; they interact with macroeconomic regimes to produce distinct patterns of accumulation. For example, the public provision of welfare in Sweden supports domestic demand with limited reliance on debt, while the liberal credit regimes of the US or UK stimulate growth through private borrowing (fueling financial instability). This comes out incredibly clearly in Wiedemann's comparison of how private debt changes for the unemployed in Denmark vs. the US:

Growth Coalitions

Behind every maintenance mechanism, and thereby any Growth Model, lies a political coalition capable of sustaining it. Growth isn’t just about what economies do — export, consume, invest — but about who benefits, who governs, and who consents. This is the insight that Baccaro, Blyth, and Pontusson (2022) bring to the forefront: the stability of a growth model depends not just on economic fundamentals but on the alignment of powerful interests and the ability to build electoral support around them.

They call this alignment a growth coalition. It's the bloc of corporate elites, government officials (elected and unelected), and organized interest groups whose policy agendas are broadly congruent. These coalitions don’t emerge from thin air. They form around specific sectors — such as finance, manufacturing, or real estate — that benefit most from the prevailing growth model.

Crucially, these actors tend to enjoy privileged access to policymakers, shaping decisions behind the scenes as much as through formal institutions.

But growth coalitions face a double challenge:

- Maintaining internal coherence, especially when constituent interests diverge.

- Winning (or neutralizing) public consent through electoral alliances, narratives, and policy tools that package elite priorities in socially acceptable terms.

As Baccaro et al. argue, growth coalitions must be "sold" to voters, even if macroeconomic policy is not strictly determined by the ballot box. Here, ideas and discourse play a key role. For example, in Germany, narratives of competitiveness and fiscal discipline help legitimize wage suppression and current account surpluses, even though the majority of workers don’t benefit directly. In Australia, by contrast, large deficits are framed as a sign of investment appeal, which shifts public perceptions about what constitutes economic success

Focusing on growth coalitions helps us understand why repeated attempts at changing a growth model end up failing. As Sierra (2022) shows in the case of Latin America, commodity-driven growth models empower rural elites, concentrate wealth, and often produce real exchange rate appreciation. That combination undermines industrial development and urban wage growth. Attempts to "switch" to more balanced models face resistance not just from global markets but from entrenched domestic interests. She illustrates these points with detailed studies of Argentina and Brazil that follow the same fundamental pattern:

| Dimension | Commodity‑Driven Growth Model | Switching Dilemma |

|---|---|---|

| Macroeconomic Policy | Generates currency appreciation | Allow the currency to appreciate (or promote devaluation) and hurt (or protect) urban and rural tradables |

| Fiscal & Regulatory Policy | Generates economic actors that hold fixed assets and concentrate income | Create an investment-friendly climate or redistribute resources to the urban sector (taxation, price controls, land reform) |

| Balance of Power | Generates structural and instrumental power of agricultural elites | Accept the veto power of the rural sector or increase the power of the urban sector |

Similarly, in Turkey and Egypt, growth model shifts— from credit-fueled consumption to export-led or investment-heavy strategies —reflect deeper reconfigurations of the growth coalition. In these cases, the relevant actors are not broad social blocs but narrower alignments of state elites and dominant capital fractions (what Güngen & Akçay term "power blocs").

These insights show that growth models are rarely technocratic. They are political projects advanced by specific actors with distinct interests. The ability of these coalitions to stabilize growth depends on how well they manage both internal contradictions and external pressures (e.g., capital mobility, currency volatility).

When and Why Growth Models Change

Growth models tend to persist. They are buttressed economically by a range of model-specific maintenance mechanisms and politically by a dominant coalition. But that does not mean they are immune to change. The analysis above indicates when change is likely to occur – when underlying growth drivers collapse, when coalitions that support them fragment, and when new political strategies emerge to rebuild legitimacy. Given that the research agenda has really only developed in the last few years, the response to the 2008 Global Financial Crisis (GFC) has turned into the focal example of such ruptures.

Fiscal Austerity and the Prospects for Realignment

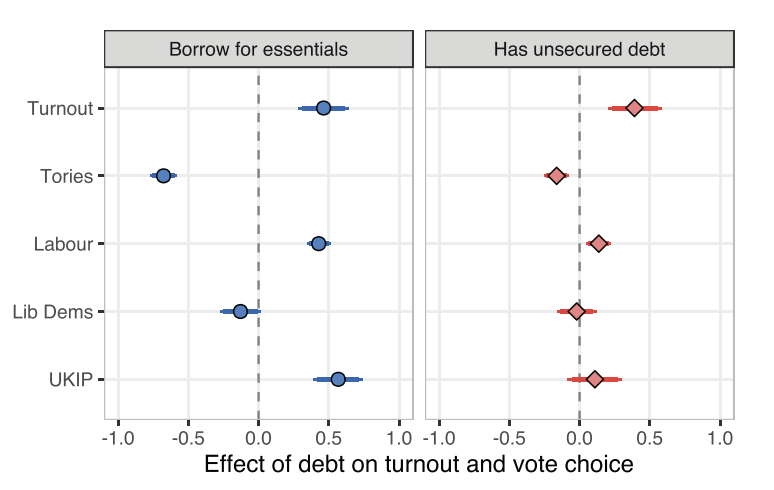

In response to the GFC only a handful of countries followed a conventional Keynesian response of fiscal stimulus (more government spending) to counter the crisis. Most — especially in Europe — adopted austerity, eventually amplifying recessionary effects. In the UK, the rollout of Universal Credit (UC) cut welfare transfers, forcing households to fill the gap with debt. This wasn't just an economic adjustment. It repoliticized private finance.

According to Wiedemann (2024), cuts to welfare benefits privatized social obligations, exposing voters to financial insecurity. In response, individuals turned to unsecured debt (credit cards, overdrafts, payday loans). Using spatial and temporal variation in the rollout of UC, Wiedemann finds a **£685 increase in unsecured debt per additional UC recipient. That may not sound like a lot on the surface but it equates to nearly a week and half of lost wages for the average person in the UK. **

The new program then triggered decline in support for incumbent Conservatives and a rise in support for Labour and UKIP, including among working-class voters.

As voters borrow to meet basic needs, they feel politically abandoned, triggering a shift from centrist parties toward both progressive and populist alternatives. That emotional groundswell creates grounds for new coalitions to emerge.

Responses to Austerity triggered the search for new coalitions

The work above indicates how coalitions can break apart as a function of how countries respond to losses in aggregate demand. Much like the US experienced in the 70s and 80s, triggering our mass wave of financialization, most governments found themselves facing legitimacy crises in the absence of growth. We saw a general pattern steadily emerge.

In democratic regimes such as Spain, Poland, and Israel, governments engaged in contingent political exchanges with labor unions, resulting in wage-boosting policies and a shift toward more domestic demand-led models. The only means of survival for the incumbent political class was to expand the coalition.

But what happens when the existing coalition refuses to budge? In hybrid regimes like Turkey and Hungary, leaders responded to growth slowdowns by instrumentalizing banking systems, expanding executive control over regulatory agencies, and repressing dissent to preserve elite coalitions and shift toward export-led accumulation under authoritarian conditions.

“This policy shift was possible because the political cost of repression was lower than the cost of redistribution.” — Apaydin (2025, p. 354)

These divergent trajectories reveal that growth model transformation depends not only on macroeconomic policy, but on the capacity of political elites to manage distributional conflict. Incorporation or coercion are both potential outcomes that then have knock-on effects for the growth trajectory of a country.

Structural and Ideational Conditions for Change

But none of that means that crises create wholesale new opportunities to redefine a growth model. The post-crisis shifts that occur are still conditioned by often global-ideational and country-specific historical factors.

One of the more remarkable and less commented on success stories of the last twenty years is Estonia’s sectoral upgrading. As Kalanta documents, the move to ICT-based growth, required long-term state commitment, institutional flexibility, and embedded public-private networks that combined a focus on both the supply side with an emerging source of aggregate demand. Unlike in the traditional East-Asian model of bureaucratic control, we saw an active revolving door between the private and public sector.

These shifts are inevitably mediated by existing party ideologies and elite visions of development. They condition what growth models are seen as legitimate and which are discarded. In moments of crisis, party narratives can repurpose failing models or craft new coalitions to sustain growth . Party incentives are the intervening step in any growth model shift.

But all of this still happens in a highly integrated global economy that conditions the choice set for how a coalition can be adapted. Relaxed external constraints — such as temporary EU leniency on fiscal rules or favorable global capital conditions - can create windows for policy experimentation, seized either by progressive reformers or autocratic elites. Or in the case of many EMs after 2008, the increasing liquidity environment allowed some governments to take over their domestic financial reigns and attempt to convert their banking sector into a new source of state-directed demand.

We can summarize some of the biggest changes, and the mechanisms behind them, based on the recent GM literature below: Conditions and Mechanisms of Growth Model Change

| Direction of Change | Example(s) | Mechanism of Change | Political Consequence |

|---|---|---|---|

| Debt-led → Political fragmentation | United Kingdom | Welfare retrenchment → rise in private debt | Electoral backlash, growth of populist opposition |

| Attempted shift to export-led → stagnation | Greece, Portugal | Internal devaluation fails to drive export competitiveness | Stagnation and political turnover |

| Demand-led → Export-led authoritarianism | Turkey, Hungary | Authoritarian control over credit and institutions | Repression of dissent, narrowing of growth coalitions |

| Export-led → Wage-boosting consumption | Spain, Poland, Israel | Cross-class political exchange with unions | Wage growth, shift toward domestic demand |

| Price-led → Non-price competitiveness | Estonia | Embedded upgrading ideology + ICT specialization | Stable growth through innovation without redistribution |

We can sum up their lessons as such:

Growth drivers are cyclical and contested. Financial booms and busts create alternating periods of growth and depression, exposing the instability of debt-led Macroeconomic crisis translates into political realignment.

Austerity-induced indebtedness fractures electoral coalitions by re-commodifying welfare and shifting risk onto households.

Growth model transitions are mediated by state capacity and ideology. The same structural shock can produce divergent outcomes—democratic incorporation, authoritarian consolidation, or technocratic upgrading—depending on political institutions and optimal coalition management .

Diminishing Drivers vs. Changing Growth Models

But it’s essential in any of these discussions to separate the failure of a model from model change. The conventional means to classify growth models looks at the different contributions to a country’s GDP on an annual basis and then treats the largest contributor for that year as the de facto GM. But that creates some strange patterns. Many economies, especially those in the Anglo-liberal and Southern European categories, experienced pre-crisis growth driven by private credit and asset inflation. But these debt-led growth models collapsed after 2008. In countries like Spain, the UK, and Ireland, household deleveraging combined with fiscal retrenchment led to sharp contractions in domestic demand.

As Kohler and Stockhammer (2022) argue this led to a categorization paradox because import compression improved current accounts. In other words, they were buying less goods and because trade’s contribution to GDP subtracts imports, these economies appear "export-led" when in fact they were simply shrinking. That growth composition risks misclassifying such cases, masking the collapse of domestic demand as export success.

The “growth driver” matters as much as the growth composition when it comes to classifying.

A major reason why I’m interested in the Growth Models approach is that it gives us an alternate vantage point to understand the green transition. In a forthcoming post, I’ll explore how the approach not only helps identify winners and losers, but also reveals how different growth models shape the coalitions, capabilities, and constraints that determine whether decarbonization strategies succeed or stall.