The Politics of Government Borrowing

Sovereign debt - bonds issued by governments - is literally the largest asset class in the world. The latest wave of globalization was undergirded by a record amount of money borrowed, and a record number of new borrowers entering global markets. Around 150 countries have tapped international investors to keep their welfare systems afloat, to build out infrastructure, or to simply avoid having to raise taxes on their citizens.

Such lending should be straightforward. A government takes money from investors, promising to pay them back — typically with interest — over time with regular annual payments built in. Standard economic fundamentals inevitably matter. Investors worry about inflation eroding returns. They track debt-to-GDP ratios, fiscal deficits, and whether borrowing is denominated in foreign currency.

But that’s barely half the story. Credibility with international markets isn’t just about the ability to pay — it’s about the willingness to pay. Government might want to inflate their way out of their commitments. Plenty of countries have simply defaulted even when their coffers have been full. Because they can. Because it makes more political sense for the incumbent.

Concerns can be avoided if you've got a long track record - if you've built up a reputation over time for not screwing over your credits. But willingness is fickle. It's harder to observe, especially over the last couple of decades when a host of new countries entered the global debt market absent a track record to fall back on. Governments don’t face the same types of enforcement as individuals or companies do, and bond investors are just as subject to the prevailing whims of the time.

In this post, I’ll unpack the two core dimensions of creating credibility: the international mechanisms that help countries win market confidence, and the domestic political structures that shape repayment behavior from within.

International Sources of Credibility

As I alluded to in the intro, one of the most remarkable aspects of the 2000s was the increase in not just the size of the bond market but the number of participants. As global liquidity soared - more money floating around in the system - borrowers from across Eastern Europe, East Asia, and Sub-saharan Africa were able to tap international markets for the first time. "In 1990, twenty-one non-OECD countries issued bonds in international markets; this number grew to forty-four by 1995. And in 2010, ninety-six non-OECD governments issued international bonds."

That left investors looking for new ways to assess governments.

Jana Grittersová's collective work shows that many lenders initially outsourced a lot of that work by relying on the decisions of foreign banks. In post-communist Europe, she finds that the presence of reputable multinational banks increases market confidence in sovereign borrowers. This isn't just about technical spillovers or regulatory upgrades. It’s reputational transfer. When Deutsche or ING sets up shop in Estonia or Hungary, investors assume the host country is safe enough for long-term bets.

Investors assume that established banks won’t behave recklessly in fragile environments because their own brands are on the line. And should crisis hit, they expect the parent to step in to rescue the subsidiary. That private safety net reduces the odds that host governments will face fiscal meltdowns or have to engineer public bailouts—both of which could imperil sovereign debt repayment. This signaling story is especially powerful in markets where hard information is unreliable or delayed.

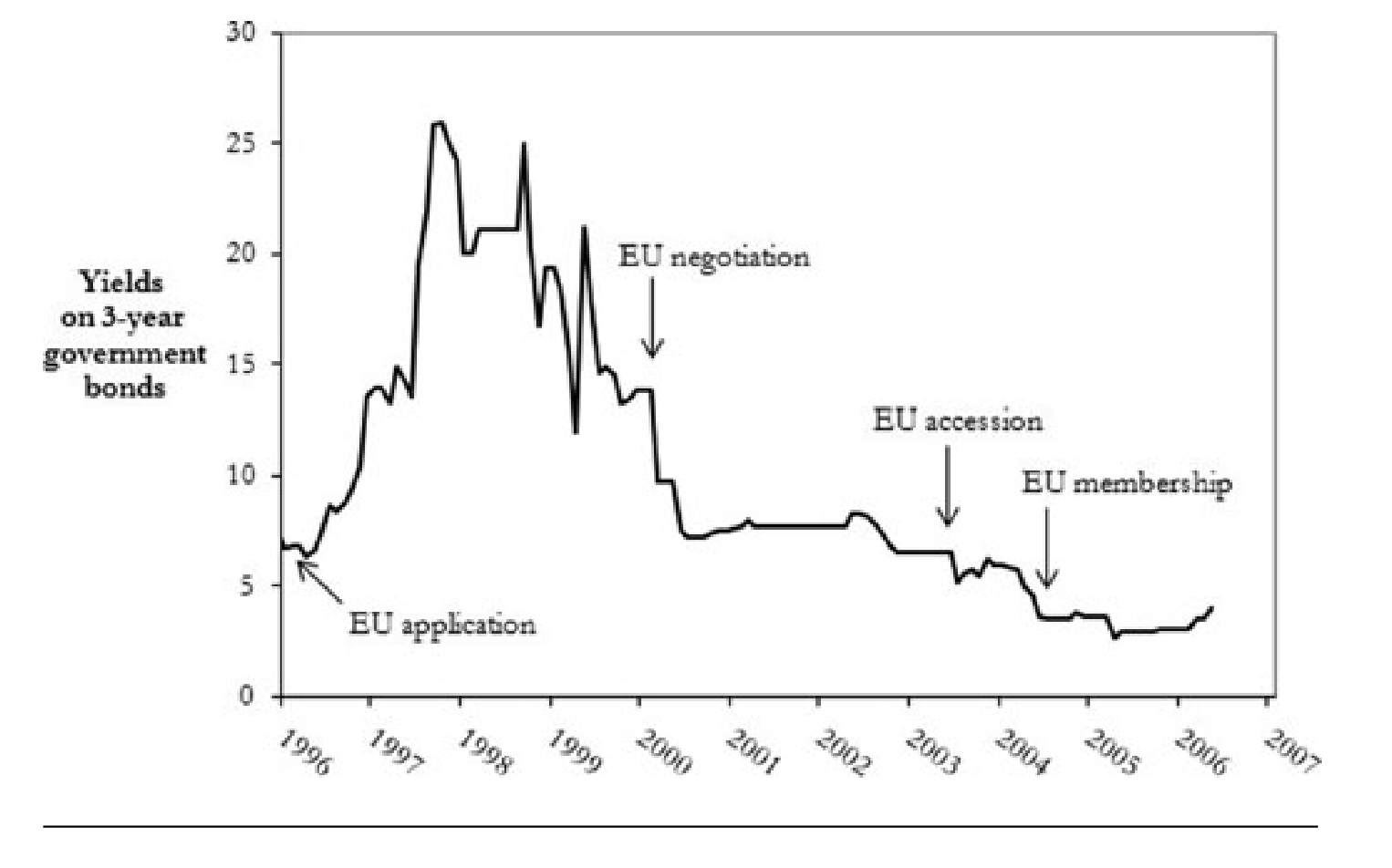

International institutions also operate as effective validators. Julia Gray (2009) finds that the European Union, through its accession process, significantly reduces sovereign borrowing costs. What matters most is not actual policy reform, but Brussels' formal acknowledgment that reforms have been "closed" at the negotiation stage. Markets respond to this official stamp of approval with lower perceived risk—even controlling for a country’s structural fundamentals.

Good enough for the EU, good enough for the bond market. As you can see from the shift in Slovak bonds spreads through the '90s and 2000s.

The effect is staggeringly large. Gray estimates that moving from the application stage to full membership drops sovereign risk by over 13 percentage points. That’s roughly equivalent to erasing the market impact of the 1998 Russian financial crisis.

Investors here are assuming that international institutional membership illustrates the type of country you are likely to be. But investors already group countries into buckets and those are hard to break out of without a major shift. Brooks et al. (2015) show the power of those categories - sovereign risk, they argue, is shaped by peer group contagion.

Countries clustered together by geography, credit rating, or market classification ("emerging markets," "frontier markets") rise and fall together in the eyes of investors. This is partly about heuristics, but also about fund incentives - many investors have specific mandates about where and who they can invest in, often clustered by the pre-defined categories.

This dynamic plays out both in moments of crisis and in everyday capital allocation. If a region is labeled unstable, all countries within it get hit with higher spreads—regardless of their actual policy stance. What happens in Argentina doesn’t stay in Argentina.

If clubs like the EU enhance credibility, the Argentina example indicates how this can backfire. In Gray's book, The Company States Keep, she shows that the depth of the alliances matter - currency union is a bigger deal than joining the same institution - and that the effect can cut both ways. Team up with a less credible set of actors, like say the Eurasian Economic Union over the European Union, and you actually lose credibility (paying more on international markets).

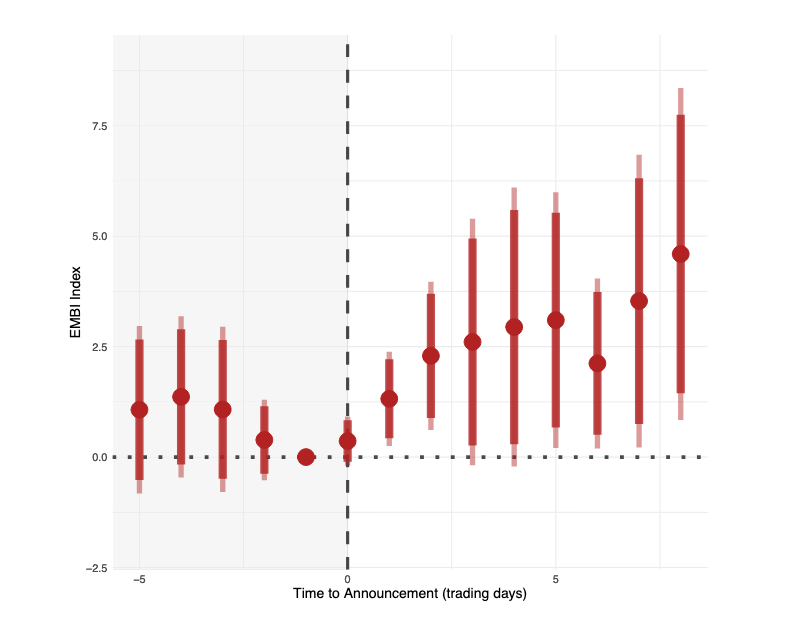

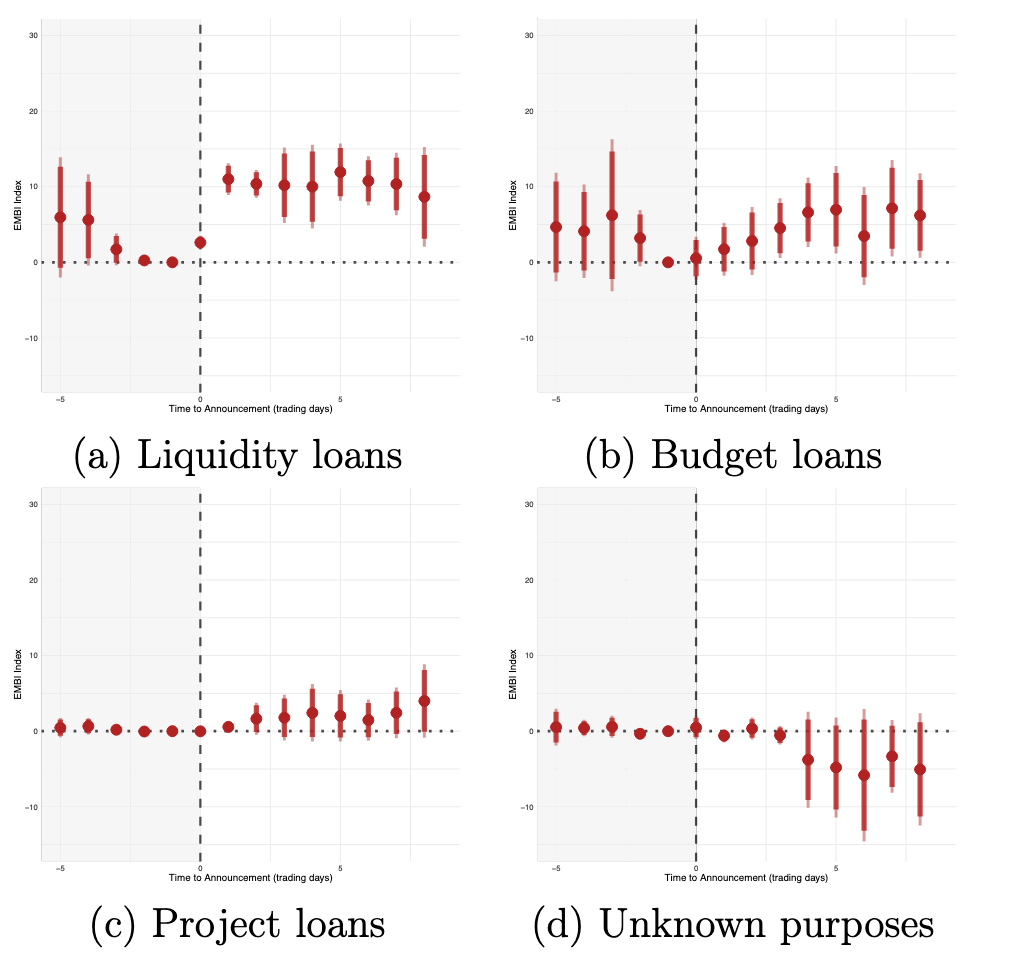

A recent working paper by Liu and Mosley show that these effects become most stark not by thinking about future associations, and instead by how bilateral financial relations are already developing. Chinese lending — especially budget support or opaque liquidity loans — raises investor concerns.

Markets punish announcements of Chinese loans with higher spreads, suggesting that creditor identity is now core to how investors assess sovereign risk. Project loans fare better than general financing, but even then, geopolitical proximity to China amplifies negative reactions. We don't see similar effects when other bailout providers step-in.

This fits into a broader story about creditor heterogeneity. Investors don't just care about total debt. They care about who you owe and under what conditions. Not all money is created equal.

The Redefinition of Original Sin

One of the most basic truths in international finance used to be that emerging markets couldn’t borrow in their own currency - investors worried that if they lent to a government in the latter's currency, they would just inflate the value away. Let's say India issued a bond at 6% interest in rupees for a one year time period. But in that year the government spent so much money that the inflation rate spike to 10%. Investors would be left holding a -4% bag (the inflation rate of 10 minus the interest they are owed.)

To avoid those situations, investors expected emerging market governments to borrow in a foreign currency they couldn't manipulate, usually dollars.

This inability to issue debt in domestic currency — what Eichengreen and Hausmann famously called original sin — was long treated as both a constraint and a curse. It meant countries had to constantly worry about exchange rates, about dollar reserves, and about whether a slight depreciation could suddenly balloon their debt burden overnight.

But that story has evolved quickly as governments learned what the market was really after. You could find credibility substitutes not to screw with inflation.

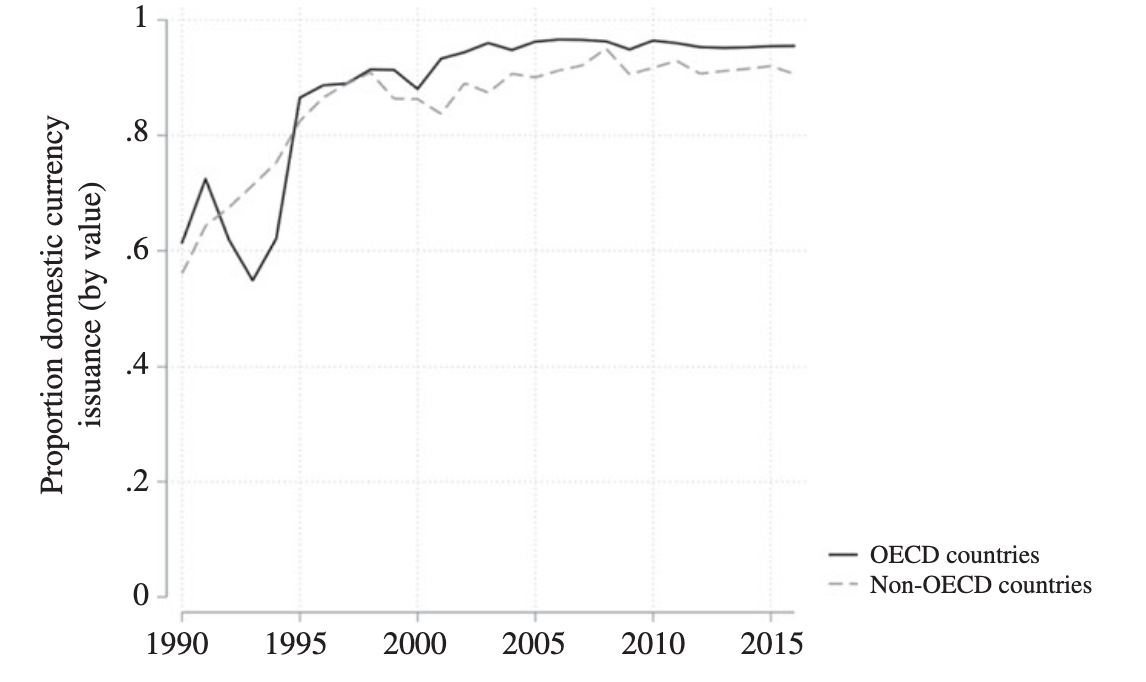

As noted, the number of non-OECD countries issuing debt exploded, from 21 in 1990 to 96 by 2010. Just as importantly, the share of bonds issued in domestic currency surged. In 1990, only 56% of non-OECD sovereign debt was denominated in domestic currency. By 2010, that number had jumped to 92%. Ballard-Rosa et al. come to these conclusions by analyzing over 240,000 bond contracts spanning more than five decades.

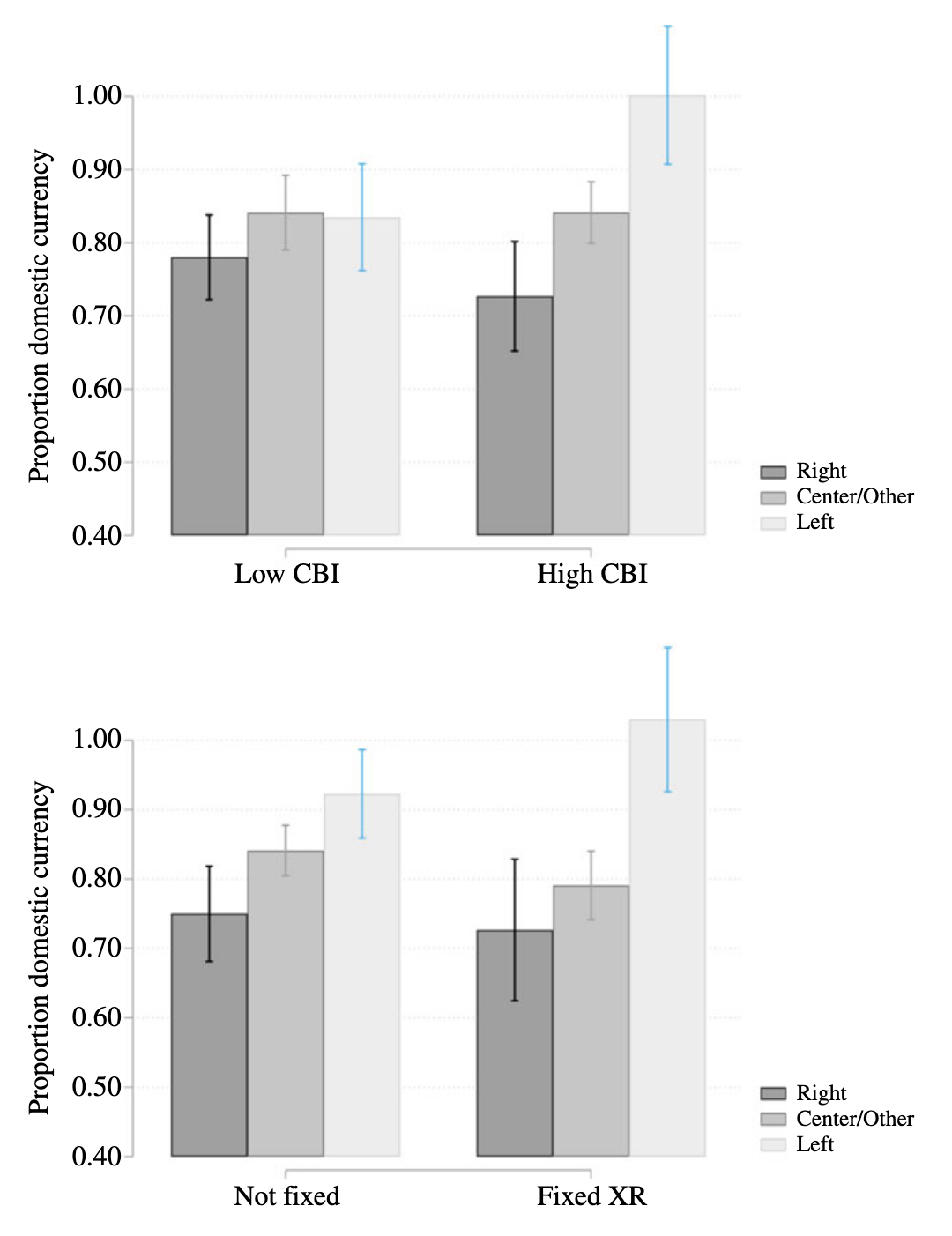

Governments of the left have shown a clear preference for domestic denomination. Per the authors, it’s because they want flexibility. Borrowing in domestic currency shifts risk to investors and preserves the government's ability to use monetary tools during crises. But that flexibility isn’t free. Investors still price in the risk. Domestic denomination often comes with higher yields or shorter maturities.

These ideological preferences do get filtered through institutional context. Left governments are most likely to borrow in domestic currency when they can point to independent central banks or credibly fixed exchange rates—institutions that assure investors that inflation won’t spiral. Think of it as credible commitment by proxy. You get the policy space, but you still have to prove you won’t abuse it.

For the right, the story flips. Right-leaning governments — more skeptical of activist macro policy — want the constraints that come with foreign currency debt. It helps tie the hands of future administrations and sends a signal of future orthodoxy. It also often aligns with the interests of domestic elites invested in financial assets.

Original sin hasn’t disappeared. It’s become conditional. Countries can shed the stigma of foreign-currency dependence, but only when other institutional features — like monetary credibility — step in to reassure investors. And that’s where we start to see the outlines of domestic structure shaping sovereign credit outcomes.

Domestic Determinants of Sovereign Credit

Before we go on, it's worth distinguishing between the ways that a lot of the coming studies examine creditworthiness. The first is usually the bond spread - what's the difference between how much a government is paying compared to a risk-free rate. That risk-free rate is usually the price of US debt since it's regarded as the most trustworthy borrower, has control of the dollar, and till recently followed a path of relative political stability and low inflation. Larger spread, more risk.

The other factor is credit ratings provided by private agencies like Moody’s, S&P, and Fitch. Governments don’t have to pay attention to them, but they do, because the market does.

Crucially, ratings aren’t updated often. Agencies aim for medium-term stability. They can’t (or won’t) change ratings every time new data rolls in, so they often build in buffers — conservative guesses about potential downside risk.

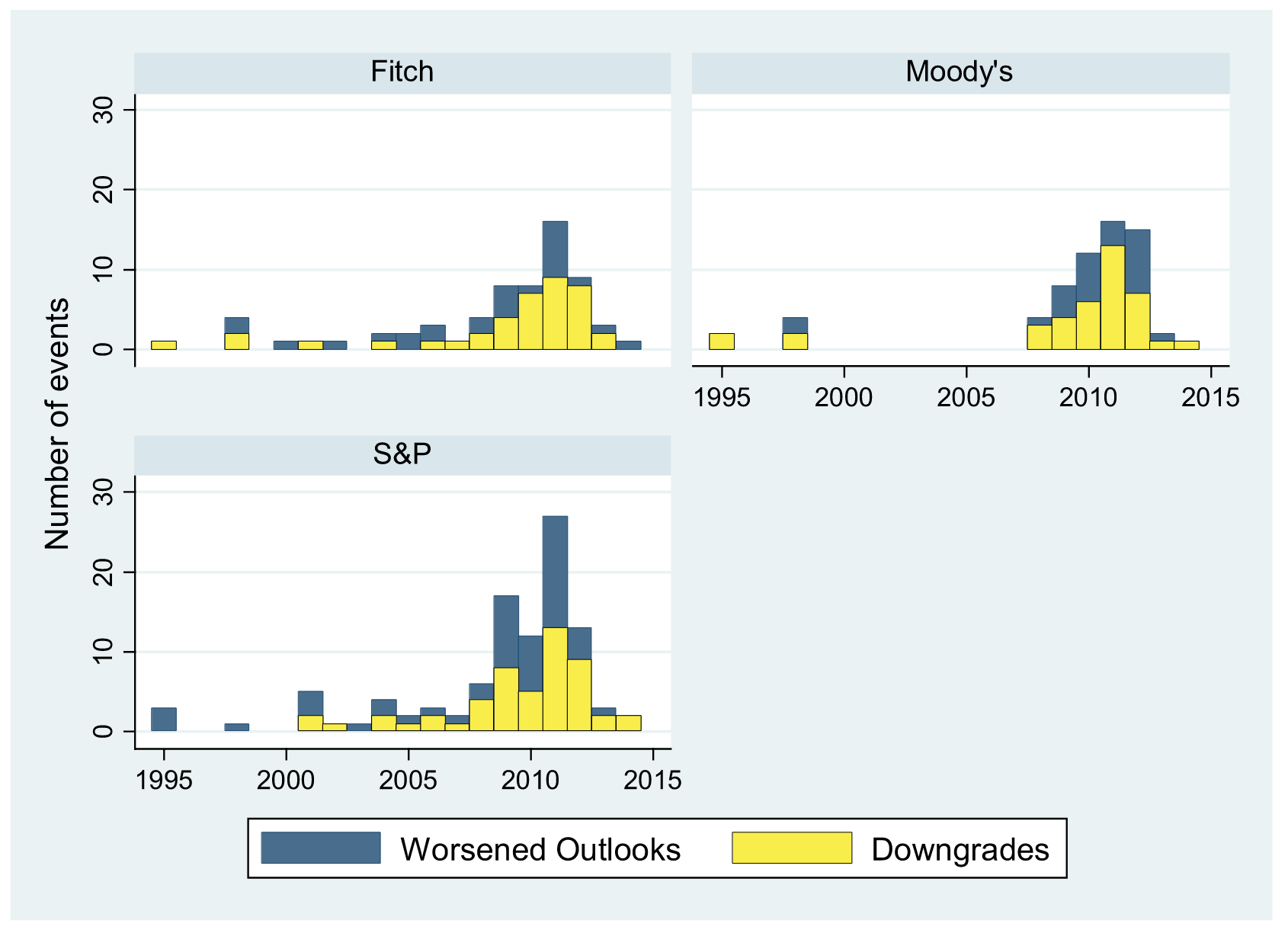

Credit rating agencies got their moment in the sunl during the 2008 financial crisis and its depiction in The Big Short. Their profit making incentives led them to not look too deep into what constituted the tranches of mortgage backed securities.

Barta and Johnston (2018) show how their economic incentives lead them to factor in political predictions. Credit rating agencies discriminate against left-wing governments — even in advanced economies where fiscal outcomes have converged across parties. Looking at data from 23 OECD countries between 1995 and 2014, they show that the arrival of left executives, especially non-incumbents, significantly increases the odds of a negative rating action — including downgrades and negative outlooks.

This isn’t about actual defaults. And it isn’t about spread reactions. In fact, markets don’t immediately penalize left governments on their own. It’s the agencies that build in ideological pessimism. Since they can’t revise ratings frequently, they’d rather err on the side of caution — assuming that left parties will be more inclined to pursue expansionary policies, raise spending, or lean heterodox. It's preemptive pricing to avoid embarrassment.

Among the big three agencies, S&P stands out. It downgraded developed economies earlier and more often during the post-2008 period, and appears most consistent in penalizing left-led governments.

These findings seem to contrast with probably the most well-known work in IPE on partisanship - Layna Mosley's work on "the room to move" which shows that investors care less about politics and more about predictability.

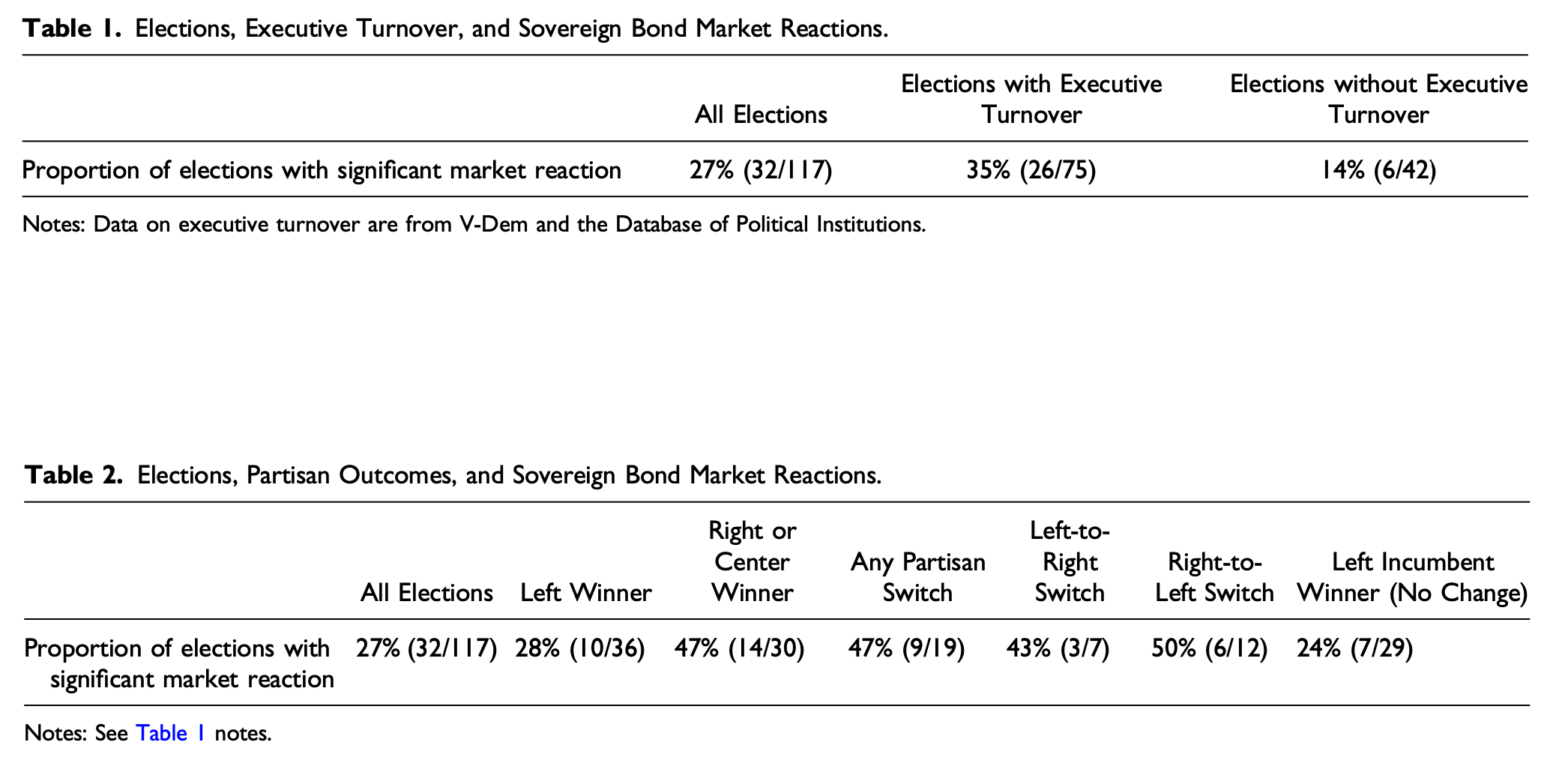

She and her co-authors usefully extend that work by using a rich dataset of 117 elections in 47 developing countries (1995–2016). They conduct an event study comparing sovereign bond spread behavior in the 90 days surrounding elections to baseline “normal” periods. Contra all the hand-ringing, most elections don’t shake markets.

Even when left governments win, the abnormal spread response is muted — just 28% of left victories see significant market movement. In fact, right and centrist wins spark more frequent market surprises.

“Markets hate the left” doesn’t hold across the board.

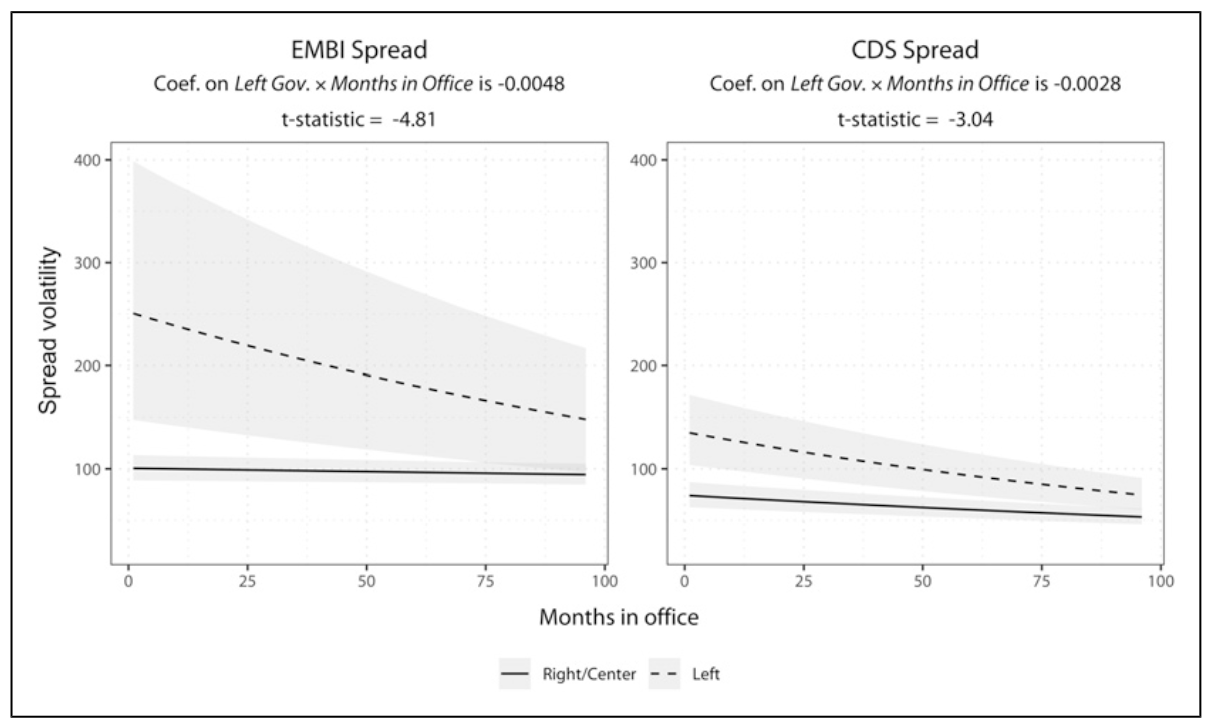

What does increase under new left governments is volatility — the day-to-day choppiness in bond spreads. Investors aren’t pricing in certain doom; they’re pricing in uncertainty. That’s especially true early in a term, before key appointments or budget decisions signal whether the new government is the “old left” or something more centrist.

This is where institutions once again kick in. The volatility effect fades faster when countries have independent central banks or fiscal rules that constrain behavior. And when global liquidity is high — think low U.S. interest rates — investors are more forgiving.

From Class to Coalitions

The papers above take a standard approach to thinking about creditworthiness, treating it like a question of class politics. Newer work is focusing more on the overall coalition that doesn't neatly fall into clean material lines. It’s increasingly a matter of cross-cutting coalitions, which align with how we've seen the left-right axis evaporate through the 2010s.

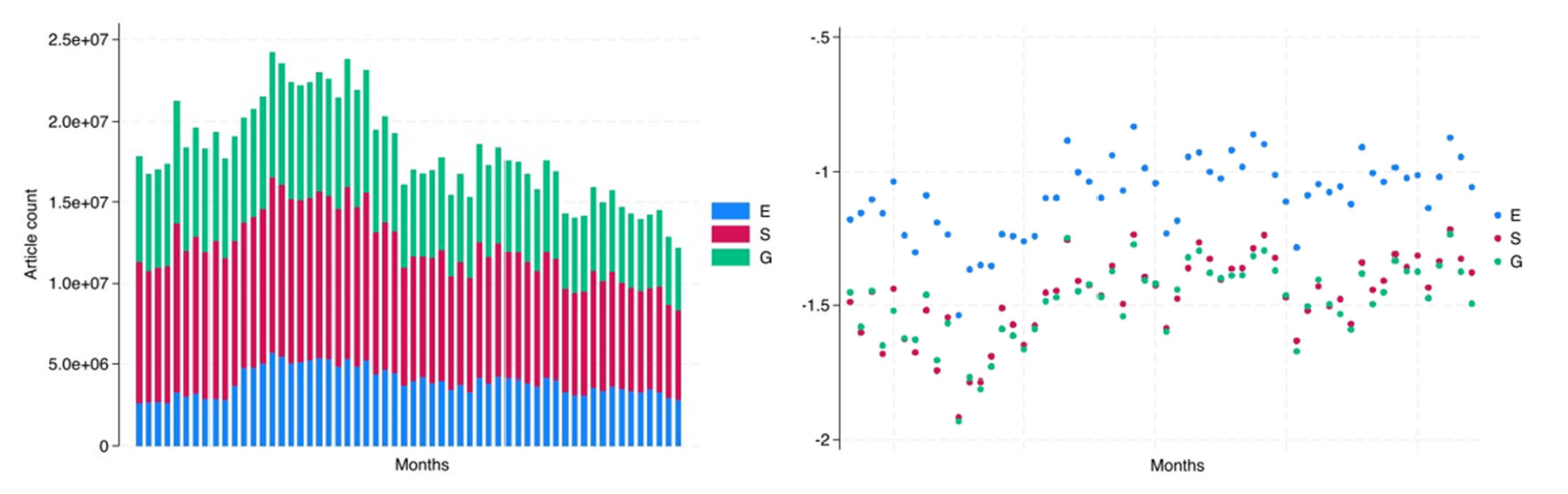

As I hope has become clear thus far, investors don't just care about the numbers but about the narrative. Jamison et al. (2025) show that sovereign credit risk is increasingly shaped by how a country is talked about — especially when it comes to ESG factors. Using machine-coded data from over 4 billion news articles globally, they construct real-time indicators of how often and how positively a government is covered on ESG issues.

The more the world’s media describes your government as environmentally responsible, socially inclusive, or institutionally strong, the better your odds of accessing capital cheaply. We can look back at the ESG wave as a bit of a farce with questionable metrics, but the news boom was real and it had an impact.

The authors use an error correction model with daily bond pricing data and find that positive ESG coverage lowers long-term sovereign spreads, even after controlling for macroeconomic conditions and political institutions.

The effect is long-run. In the short term, markets struggle to incorporate ESG data cleanly. But over time, sustained positive messaging about environmental or governance performance becomes part of the sovereign risk profile. And that effect is strongest in industrialized democracies — where both supply and demand for ESG information are high.

This brings us to back to the broader theme. Investors are getting more politically sophisticated. They seem to plausibly even be reading the political science.

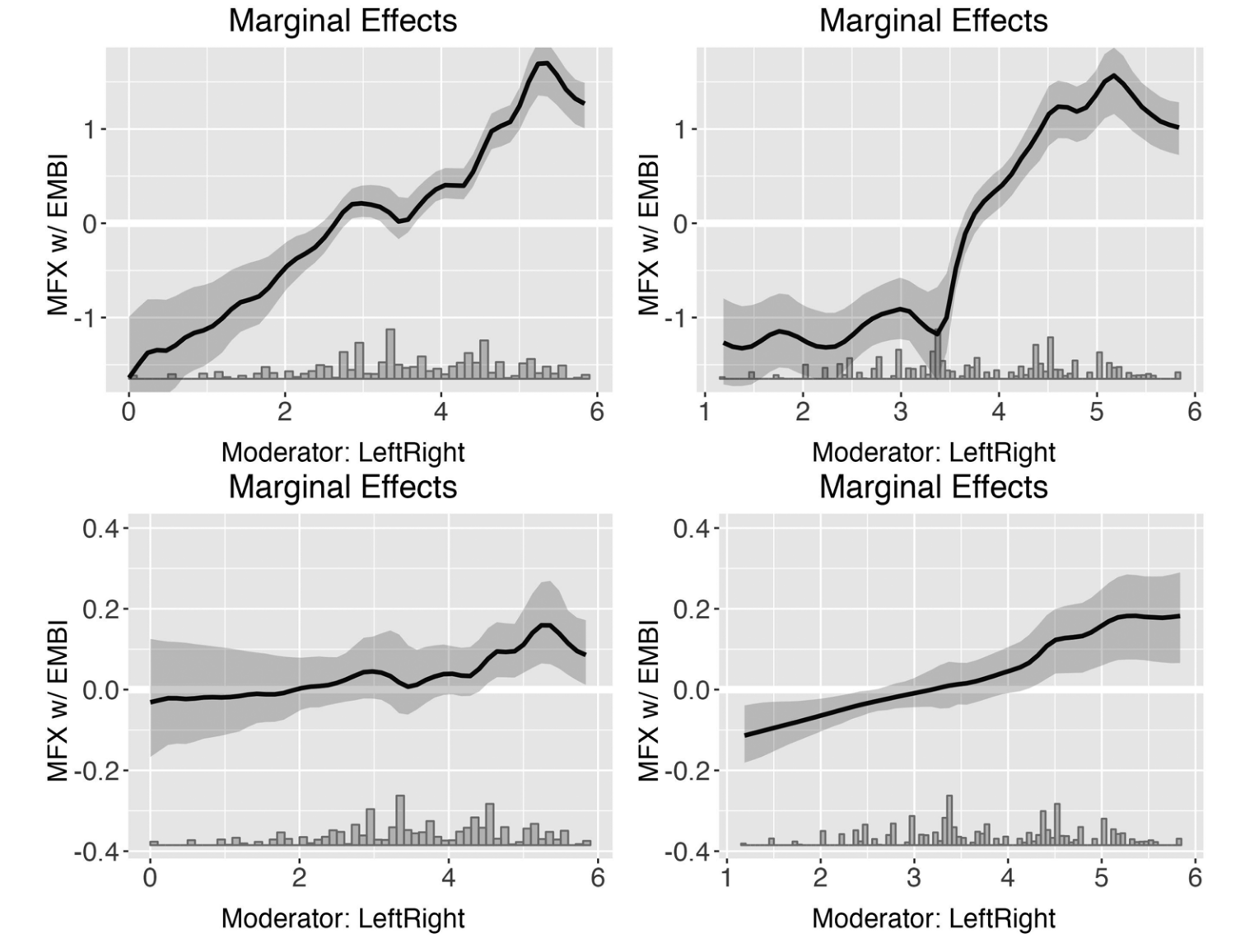

That’s the focus of Brown et al. (2024), who argue that coalition structure — particularly along ethnic lines — plays a pivotal role in shaping perceived sovereign risk. Historically, the left was assumed to spend more, making them riskier to creditors. But Brown and colleagues find that the social basis of a government’s base can invert those expectations.

When left governments rely on ethnic support, they tend to have smaller winning coalitions - fewer people they need to keep happy to stay in power - and therefore fewer broad-based entitlements to maintain. That gives them greater fiscal flexibility and makes them more creditworthy in the eyes of investors.

In contrast, right governments with ethnic bases often face pressure to deliver targeted goods to specific constituencies, which can erode the very fiscal discipline markets expect from the right. In those cases, bond spreads increase, reflecting elevated perceived risk.

The effect sizes are not subtle. A one-standard-deviation increase in ethnic support reduces spreads (cheaper money) by 22% for far-left governments but increases spreads by 41% for far-right ones, holding other fundamentals constant. This isn’t about total spending levels, but about the flexibility of those commitments — a distinction that credit rating agencies are increasingly attuned to.

As we'll see in the next post, that reputational logic also applies to formal institutions. Coalitions are not just constrained by what voters demand, but by how rules — particularly the functioning of democratic institutions — shape expectations about how credible those demands really are.